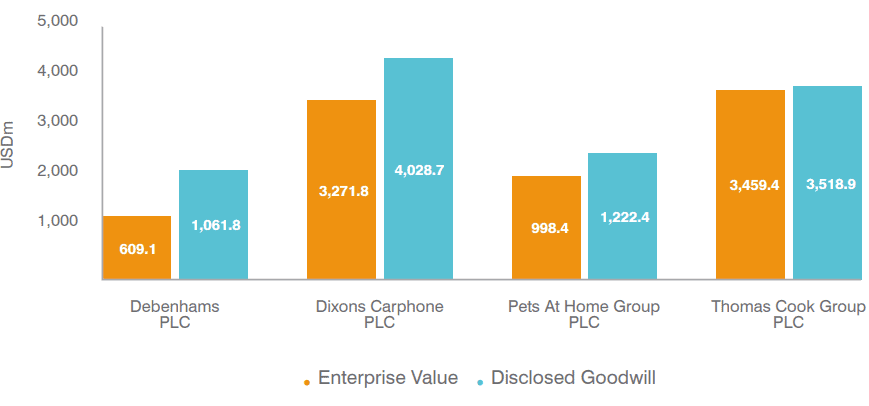

No artigo "Negócios de risco: o tratamento contábil do ágio", Publicado em 2018, comentei a resistência generalizada à divulgação de ativos intangíveis específicos. Mais comumente, o valor excessivo reconhecido na aquisição de uma subsidiária é agrupado na classe de ativos intangível ambígua, a boa vontade.

Na análise, observei o valor de boa vontade reservado versus o valor total da empresa para quatro principais redes de marca do Reino Unido: Debenhams, Dixons Carphone, Pets em casa e Thomas Cook Group.

So how did 2019 turn out for these 4 companies?

Debenhams

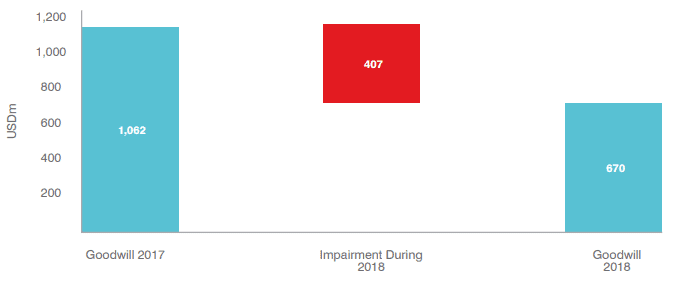

Logo após a conclusão da análise de white paper no ano passado, o novo diretor de Finanças de DeBenhams levou um prejudicação do Branco de US $ 407, que contribuía com o impacto do Branco de US $ 40. Dividendos. Alguns atribuem a situação de Debenhams com o fracasso em se adaptar a um cenário competitivo em mudança e à queda da confiança do consumidor. Embora altos níveis de boa vontade não tenham sido a causa direta dos problemas de Debenhams, o tratamento histórico contábil não ajudou a situação.

Subsequently in 2019, Debenhams entered into a CVA. Some attribute Debenhams’ situation with a failure to adapt to a changing competitive landscape and falling consumer confidence. While high levels of goodwill were not the direct cause of Debenhams’ issues, the historic accounting treatment did not help the situation.

O ágio é ambíguo e, portanto, desafiador de interpretar, sem o conhecimento total do modelo subjacente ao seu cálculo e teste anual de comprometimento. Isso fornece evidências adicionais que apoiam nossa visão de que a avaliação específica de ativos intangível deve ser conduzida por especialistas independentes, antes e nos anos após uma aquisição significativa. ano a ano. Enquanto a boa vontade ainda excede o valor da empresa, um comprometimento de US $ 294 m é refletido na nova figura de boa vontade. O comprometimento foi causado por uma taxa de desconto mais alta aplicada na avaliação do teste de redução ao valor recuperável, refletindo maior incerteza e desafios para o ambiente de varejo do Reino Unido. A posição do grupo melhorou ano após ano, o valor da empresa cresceu 53%e a empresa excedeu repetidamente as expectativas dos analistas. Para melhorar a transparência para analistas e investidores, avaliadores de ativos intangíveis especializados devem ser consultados antes, durante e após uma transação. Praticantes como o financiamento da marca podem ajudar a aconselhar e fornecer uma opinião sobre o valor dos ativos intangíveis em questão, bem como recomendações sobre como aumentar esses valores de ativos em todo o plano de integração. Após, a gerência executiva ficou escrutínio para os altos salários e 20 milhões de libras em bônus nos últimos 5 anos - apesar das indicações das lutas da empresa. Idealmente, Thomas Cook nunca deveria ter reconhecido um valor tão alto para a boa vontade. Esse valor de boa vontade surgiu devido à série de aquisições entre 1993 e 2011. Esse valor poderia ter sido alocado para outros ativos além da boa vontade, como marca, tecnologia, valor contratual ou mesmo valor de relacionamento com o cliente.

Dixons Carphone

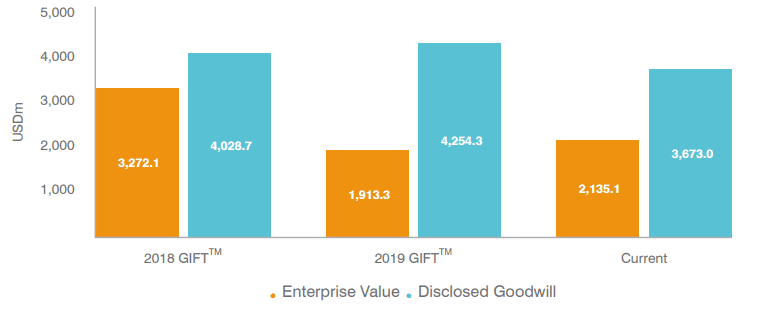

In the 2019 analysis, Dixons Carphone’s proportion of goodwill to enterprise value remained high, especially given that the latter fell further, by 42% year-on-year.

Subsequently to this year’s GIFT™ analysis, Dixons released their 2019 financial results. While goodwill is still in excess of enterprise value, an impairment of $294 m is reflected in the new goodwill figure. The impairment was caused by a higher discount rate applied in the impairment test valuation, reflecting higher uncertainty and challenges for the UK retail environment.

Pets at Home

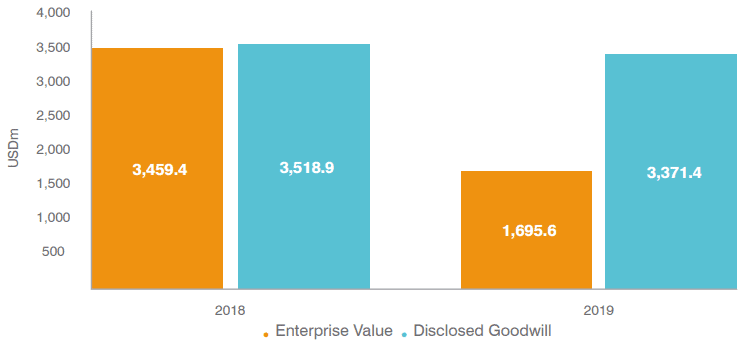

A slightly different tale for Pets at Home; the group position has improved year on year, enterprise value has grown by 53%, and the company has repeatedly exceeded analyst expectations.

If such high goodwill was avoided in the first place, perhaps investors would have understood the future viability of the company, thus maintaining holdings and the share price. To improve transparency for analysts and for investors, expert intangible asset valuers should be consulted before, during, and following a transaction. Practitioners such as Brand Finance can help to advise and provide an opinion on the value of intangible assets under question, as well as recommendations on how to grow those asset values throughout the integration plan.

Thomas Cook

Having failed to gain sufficient backing for a £900m rescue deal, Thomas Cook collapsed in September 2019. As a result, 150,000 British holidaymakers were stranded overseas. In the aftermath, executive management came under scrutiny for the high salaries and £20m in bonuses over the past 5 years – despite indications of the company’s struggles.

When Brand Finance conducted this year’s GIFT™ analysis, right before the company collapsed, the last reported goodwill was just shy of two times the enterprise value. Ideally, Thomas Cook should have never recognised such a high value for goodwill. This goodwill value arose due to the series of acquisitions between 1993 and 2011. This value could have been allocated to other assets than goodwill, such as brand, technology, contractual value, or even customer relationship value.

No início de 2019, as finanças da marca avaliaram a marca Thomas Cook em 836 milhões de libras. No início de novembro, o conglomerado chinês Fosun adquiriu as marcas registradas Thomas Cook, sites, contas de mídia social e software em quase todos os mercados globalmente por apenas 11 milhões de libras. No entanto, Thomas Cook é uma das muitas marcas britânicas que foram retiradas por preços de barganha porque a gerência não conhece todo o valor. Para proteger os principais ativos, a primeira etapa -chave é entender seu valor para os negócios e como apoiar esses ativos. Isso deve ser feito antes, durante e após a aquisição. Valores específicos de ativos intangíveis, como a marca, devem ser considerados por meio de uma lente legal, comportamental e financeira. Este exercício força os ativos intangíveis a serem objetivamente avaliados, fundamentados na realidade das percepções reais das partes interessadas e do desempenho dos negócios. É oferecido adquirido aos investidores, há um caso adicional para a divulgação de valor intangível. Atualmente, intangíveis gerados internamente, como o valor da marca, não podem ser capitalizados e divulgados no balanço. Idealmente, todos os ativos intangíveis, adquiridos e gerados internamente, devem ser reavaliados a cada ano, e os conselhos devem ser obrigados a divulgar sua visão desses valores. Liderança

The brand was undeniably troubled – even before the 2019 reputational damage, Thomas Cook faced existing competition from DIY holiday sites including Skyscanner, Airbnb, Booking.com, and Trivago. However, Thomas Cook is one of many British brands that have been scooped up for bargain prices because management don’t know their full worth.

Lessons

We all know that M&A is tricky, with many business combinations failing. To safeguard core assets, the first key step is to understand their value to the business, and how to support those assets.

Management needs to consult with independent, objective subject experts to determine the value of their intangible assets. This should be done pre-, during and post-acquisition.

This would help management to integrate a target company successfully. Specific intangible asset values, such as brand, should be considered through a legal, behavioural, and financial lens. This exercise forces the intangible assets to be objectively appraised, grounded in the reality of actual stakeholder perceptions and business performance.

By properly recognizing the value of specific intangibles, rather than lumping it all into goodwill, users of financial statements are able to better scrutinise the specific intangible assets expected to bring value to the business.

If deeper insight into the specific intangible assets acquired is offered to investors, there is a further case for intangible value disclosure. Currently, internally generated intangibles such as brand value cannot be capitalised and disclosed on the balance sheet. Ideally, all intangible assets, both acquired and internally generated, should be revalued every year, and boards should be required to disclose their view of those values.