Este artigo foi publicado originalmente no Brand Finance Gift ™ 202 Relatório. Consistente com esta missão, também exploramos certos problemas emergentes que acreditamos ser impedimentos sistêmicos para nossas partes interessadas da profissão de avaliação e também aos mercados de capitais em geral.

At the International Valuation Standards Council (IVSC), our mission is to develop and propagate a truly global set of valuation standards to the benefit of the capital markets and all its stakeholders. Consistent with this mission we also explore certain emerging issues which we believe are systemic impediments to our valuation profession stakeholders and also to the capital markets at large.

Diretor Técnico,

IVSC & Gerenciando

Diretor, BDO

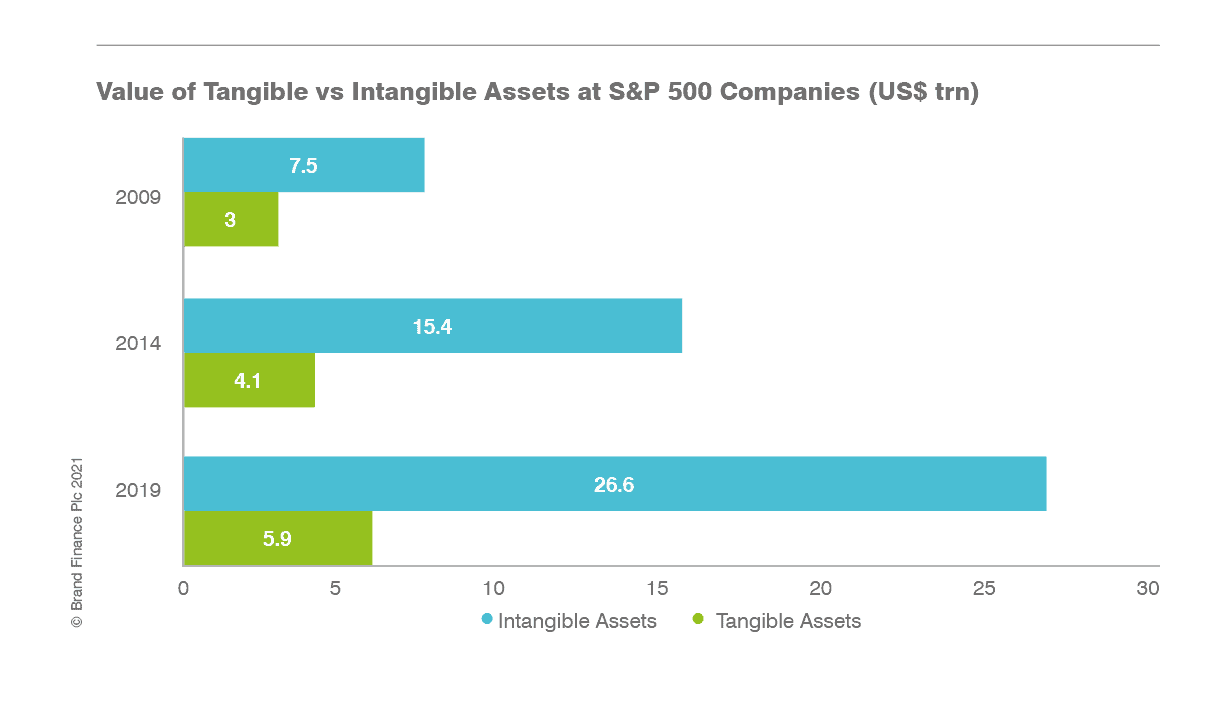

Fazemos isso através de pesquisas e publicações de liderança de pensamento, engajamento de partes interessadas e compartilhamento de perspectivas por meio de reuniões públicas, e webinars. Recentemente, começamos a trabalhar em uma questão de grande importância, explorando a necessidade e as oportunidades dos padrões de relatórios financeiros para se alinhar melhor ao papel dos ativos intangíveis na economia moderna. O investimento em ativos intangíveis, gerado internamente e por aquisição, é fundamental para o processo de alocação de capital de uma empresa. Da mesma forma, a capacidade dos investidores de identificar essas empresas mais capazes de traduzir esses investimentos em retornos de longo prazo é igualmente crítica. O IVSC suporta financiamento da marca e todos os outros, que procuram progredir nessa questão mais crítica. transação de terceiros. Como muitos modelos de negócios atuais evoluíram ao longo de décadas, a saber, para confiar mais em ativos intangíveis às custas de tangíveis, os padrões para relatar essa atividade não. Como resultado, a economia e os padrões de relatório tornaram -se desalinhados. Na demonstração do resultado, a despesa imediata ignora o princípio correspondente que governa quase todas as outras atividades corporativas. Em reação, muitas empresas optam por comunicar várias medidas não-GAAP que se ajustam a essa atividade. Além disso, a falha em reconhecer intangíveis gerados internamente significa que esses investimentos são amplamente excluídos dos ecossistemas de governança, relatórios financeiros e auditoria. Portanto, esses investimentos têm menos probabilidade de ter divulgações correspondentes ou serem incluídos na discussão e análise da gestão (MD&A) e, portanto, menos propensos a receber escrutínio dos auditores ou serem visíveis para os investidores. Esse desconexão também permeia através dos processos de teste de redução ao valor recuperável, pois a boa vontade adquirida e os intangíveis pode ser protegida de reduções de redução ao valor recuperável por boa vontade e intangíveis desenvolvidos internamente e intangíveis que não são refletidos no balanço

Intangible assets have long been the engine for value creation in the world’s developed economies. The investment in intangible assets, both internally generated and through acquisition, is critical to an enterprises’ capital allocation process. Similarly, investors’ ability to identify those enterprises best able to translate such investments into long-term returns is equally as critical.

Brand Finance has been lobbying for greater intangible asset disclosure for about 20 years now. The IVSC supports Brand Finance, and all others, that look to make progress on this most critical issue.

Kevin Prall, Technical Director, IVSC & Managing Director, BDO

The Case for Realigning Reporting Standards with Modern Value Creation

Despite the importance of intangible assets to the capital markets, only a small percentage are recognised on balance sheets, typically via acquisition from a third-party transaction. As many current business models have evolved over decades, namely, to rely more heavily on intangible assets at the expense of tangible, the standards to report on such activity have not. As a result, the economics and the reporting standards have become misaligned.

This misalignment has ripple effects through the financial statements. In the income statement, immediate expensing ignores the matching principle that governs nearly all other enterprise activities. In reaction, many companies choose to communicate various Non-GAAP measures that adjust for such activity. Additionally, failure to recognise internally generated intangibles means that such investments are largely excluded from the governance, financial reporting, and auditing ecosystems. Therefore, such investments are less likely to have corresponding disclosures or be included in the management discussion and analysis (MD&A), and therefore less likely to receive scrutiny from auditors or be visible to investors.

There are also practical implications for specific accounting standards, none more obvious than the disconnect between acquired intangible assets and certain internally-developed intangible assets. This disconnect permeates through the impairment testing processes as well, as acquired goodwill and intangibles can be shielded from impairment write downs by internally-developed goodwill and intangibles that are not reflected on the balance sheet 1 || 121 . All told, such limitations have caused many to question the relevance of financial statements in the modern economy 2. Por exemplo, em O final da contabilidade e o caminho a seguir para investidores e gerentes Os autores, Baruch Lev e Feng Gu, * Segundo o poder explicativo dos ganhos relatados e do valor contábil entre 1950 e 2013. O poder explicativo dos ganhos relatados e o valor contábil no valor de mercado) caiu de aproximadamente 90% para 50% no período2 (i.e., the explanatory power of reported earnings and book value on market value) declined from approximately 90% to 50% over the period 3.

Many have noted this severe disconnect between market values and book values (i.e., the unidentified intangible asset value) 4. PER O balanço patrimonial desequilibrado: fazendo com que os intangíveis contem, o valor de ativo intangível não registrado cresceu exponencialmente de 2009 a 2019.

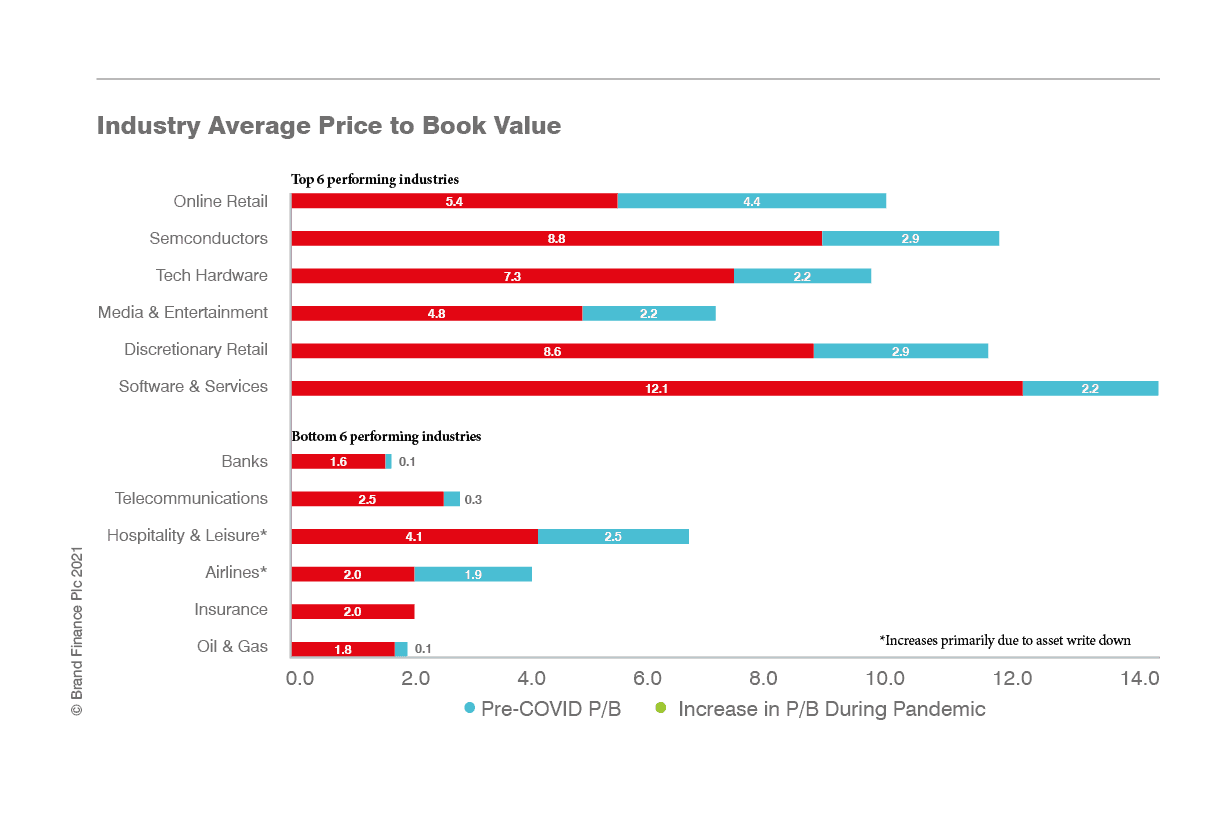

Beginning in 2020, the pandemic acted to further accelerate this long-standing trend, particularly for those industries most reliant on intangible value creation, as it has fundamentally changed how people live and work 5. Um trecho de uma análise recente que analisou 24 indústrias separadas mostra que os valores de mercado aumentaram mais de fevereiro de 2020 a maio de 2021 para as empresas que já tinham o maior valor de mercado para os múltiplos de valor de reserva. Para mostrar a aceleração da tendência em 2020 e 2021, o gráfico abaixo exibe o preço do valor contábil para as 6 principais indústrias de performance e as 6 indústrias de performance. O IVSC suporta financiamento da marca e todos os outros, que procuram progredir nessa questão mais crítica.

This confirms that the pandemic has further exacerbated the disparity between market values and book values for those industries most reliant on brands, technology, and human capital for value creation. The IVSC supports Brand Finance, and all others, that look to make progress on this most critical issue.

REFERÊNCIAS

- Para mais detalhes, consulte: Documento de Perspectivas IVSC, Valor da informação do teste de comprometimento atual (maio de 2020) || Resposta do Instituto↩

- Invitation to Comment (ITC) Identifiable Intangible Assets and Subsequent Accounting for Goodwill - CFA Institute Response, janeiro de 2020. Veja também: Contabilidade hoje, Custo versus valor: GAAP está obsoleto? (December 2020) ↩

- The End of Accounting and the Path Forward for Investors and Managers, Wiley (June 2016) ↩

- Para fins desta discussão, assumimos que substancialmente todo o prêmio do mercado sobre o valor contábil se deve a ativos intangíveis não reconhecidos. No entanto, observamos que uma porção menor do prêmio é frequentemente atribuída a ativos tangíveis, pois muitos dos regimes de depreciação em todo o mundo permitem ou exigem depreciação contábil que supere a depreciação econômica real. A hospitalidade e o lazer e as companhias aéreas aumentam em P/E são em grande parte devido às reduções no valor contábil, à medida que ocorreram redes e aposentadorias significativas durante a pandemia. Poder com inovação e liderança digital↩

- BDO, The Path Ahead, Analysis of Analyst Estimates for Insights on the Economic Recovery, pages 23-25. Hospitality & Leisure and Airlines increases in P/E are largely due to the reductions in book value, as significant asset write downs and retirements occurred during the pandemic.↩