Covid abalou a indústria automobilística, mas as perspectivas de longo prazo parecem positivas. O investimento está por trás da mudança para a energia elétrica, mas o marketing e o posicionamento da marca precisam recuperar o atraso. Alex Haigh nos diz mais.

- O que está acontecendo com a indústria? Com planos de investimento maciços

- 2020/21: A Rollercoaster Year

- Resilience for Long-Term Brand Value

- Restructuring in The Automotive Industry

- Regulatory Pressure to Invest in Electric

- Car Companies Responding With Massive Investment Plans

- Mudar para a mudança elétrica da paisagem da marca

- Gastes de marketing Tomando um golpe

- Novas abordagens para concessionárias e propriedade

- O que tudo significa que tudo significa que tudo significa que tudo significa que tudo isso significa que tudo isso significa que tudo isso significa que tudo isso significa que tudo significa que tudo isso significa que tudo isso significa que tudo isso significa que tudo isso significa que tudo isso significa que tudo isso significa que tudo isso significa que tudo está acontecendo na indústria? Modelos de negócios existentes sob tensão e aumento da indústria.

What Has Been Happening To the Industry?

The mobility industry is currently undergoing profound changes, both short and long term, that are putting existing business models under strain and upending the industry.

Marcas automotivas estão sendo influenciadas pela crise Covid; a crise climática e a mudança para carros elétricos; uma relação em evolução entre sociedade, pessoas e carros; mudanças nos padrões de deslocamento; mudanças na propriedade do carro; E mesmo os lentos, mas sempre presentes, passam em direção a veículos mais autônomos. Ano

The list is dizzying but despite these fundamental challenges and the rise of extraordinary new competitors like Tesla, the signs point to a resilient sector ready and able to meet the challenges in front of it.

2020/21: A Rollercoaster Year

Sendo uma das indústrias mais globalizadas do mundo, a indústria automotiva pegou o frio Covid rapidamente. Ásia -Pacífico e, mais tarde no trimestre, na Europa. Euromonitor. No trimestre 3, a Volkswagen-que deve ser observada tem participação de mercado significativa na China-já estava registrando as vendas trimestrais quase equivalentes ao mesmo trimestre em 2019.

In Q1 for example – before lockdowns were put deeply in to force in Europe and the Americas – Volkswagen Group was already registering around a 25% reduction in sales and production compared to the same quarter in 2019 due to crashing demand in Asia Pacific and, later in the quarter, in Europe.

As the effects of lockdowns rippled across the world from China between January and August of 2020, all car brands were badly affected with sales for many brands dropping by over 30% or 40% compared to the same quarter 2019.

The year has been destructive and we have seen unit sales drop by over 16% in 2020 compared to 2019 to levels not seen since 2011, according to Euromonitor.

However, as countries in the Asia Pacific begin to get the health crisis under control and protect their citizens from the COVID-19 virus, growth started up again – in some cases strongly. By quarter 3, Volkswagen – which must be noted has significant market share in China – was already registering quarterly sales almost equivalent to the same quarter in 2019.

tudo isso apontou para brotos verdes de uma recuperação, embora de maneira fortemente dependente de um que pode ser imaginado. Valor

Resilience for Long-Term Brand Value

Avaliações de marca, como em qualquer tipo de valor comercial ou ativo, são uma aposta educada no futuro. Eles determinam de onde virão os ganhos relacionados à marca, analisando como os pontos fortes das marcas influenciarão a demanda no futuro e de onde-em um nível de mercado-de que a demanda virá. Valor total da marca para o

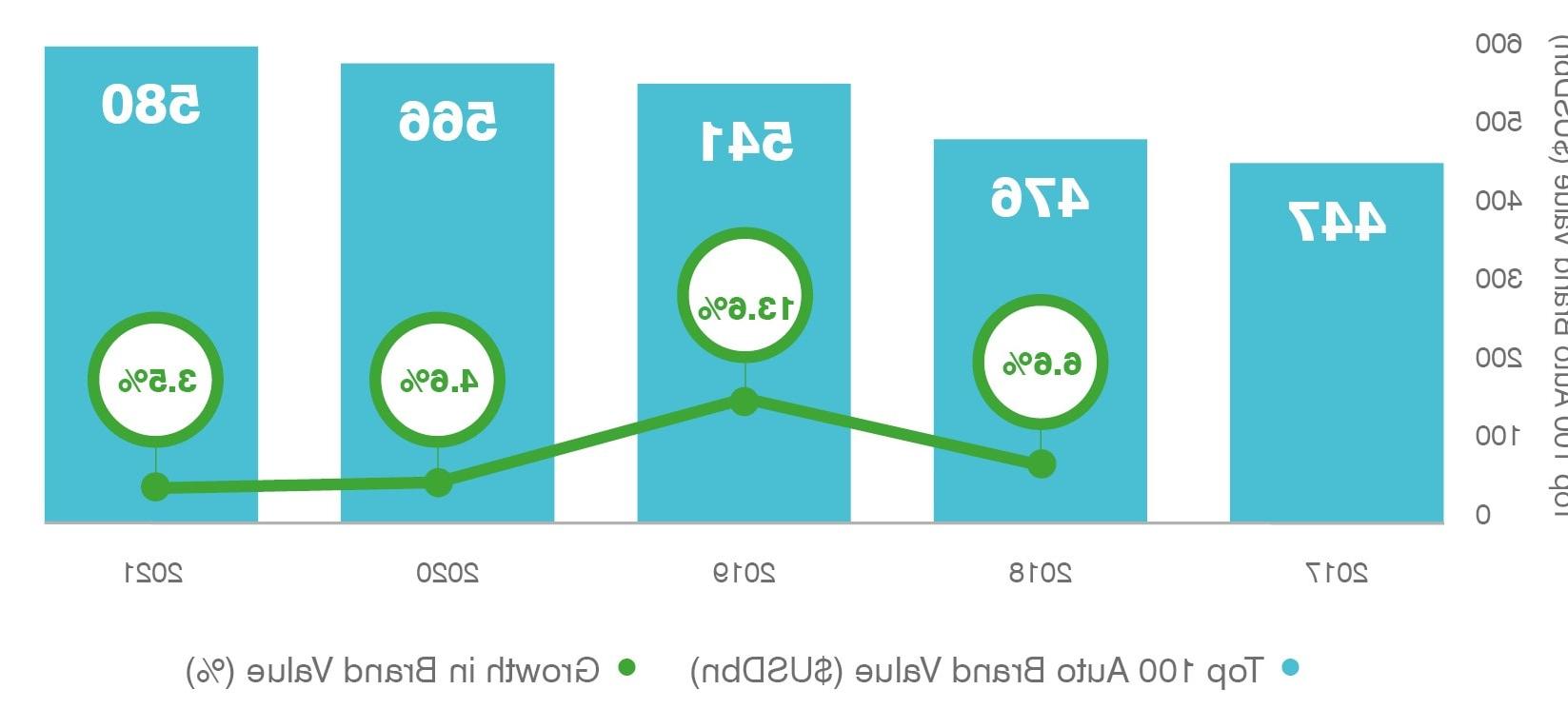

Despite the past year, our view is that the outlook for the industry looks in fairly good shape. Total brand value for the Tabela de automóveis é o mais alto que já esteve em US $ 586 bilhões em valor - quase o dobro do valor da Oil & Gas= Indústria e 6 vezes o da indústria de companhias aéreas. No entanto, o crescimento ano a ano diminuiu este ano. De uma forte posição em 2019, 2020 e 2021 viam crescimento suave de valor, pois as pressões sobre comércio e crescimento internacionais adotaram mordidas da demanda pouco antes, mas particularmente durante o ano inicial da crise Covid. Como resultado, as marcas na indústria automobilística estão realmente se tornando cada vez mais importantes na mistura geral-atingindo uma alta de cinco anos de 7,3% do valor total da marca do nosso

That being said, this drop in growth comes on the back of slower global growth for all industries. As a result, brands in the automobile industry are actually becoming more and more important in the overall mix – reaching a five-year high of 7.3% of the total brand value of our TOP 500 MAIS VALIÁRIAS BARDS GLOBAL TABELA 2021. mais rápido.

Growth is coming from diverse sources but generally those brands with more exposure to China and Asia Pacific, along with SUVs, electric vehicles and commercial trucks – which have benefited from a surge in road freight demand – are tending to grow fastest.

This all means that Tesla, our fastest growing brand, is accompanied both by its Chinese rival NIO and also by more traditional brands like RAM Trucks, Jeep, Lincoln, and Dodge na lista das 10 principais marcas de crescimento mais rápido este ano. O termo de pesquisa "CAR" caiu significativamente na popularidade mundial durante os primeiros bloqueios, subindo para os níveis de 2019 no outono e caindo com as terceiras ondas de Covid. Nos dois primeiros meses do ano, eles ficaram deprimidos e ainda não chegaram aos níveis de 2019. Desde o início de 2019, sua popularidade mais que dobrou. "4x4", que é coincidentemente quatro vezes mais popular que o "carro elétrico", também aumenta - embora apenas em cerca de 20%. Por outro lado, hatchbacks, sedãs e outros modelos não estão vendo esse nível de crescimento. Essa mudança gradual será o desafio definidor para todas as marcas de automóveis tradicionais.

Taking a look at leading indicators, for example search trends, helps unravel some of these trends in passenger cars. The search term “car” dropped in worldwide popularity significantly during the first lockdowns, rising to 2019 levels in the autumn and falling with the third waves of COVID. For the first two months of the year they have been depressed and have not yet reached back up to 2019 levels.

“Electric car” on the other hand has more or less not stopped rising. Since the start of 2019, its popularity has more than doubled. “4x4”, which is coincidentally four times more popular than “electric car”, is also up – albeit only by about 20%. On the other hand, hatchbacks, sedans and other models are not seeing this level of growth.

However, while these trends are compelling and directional, it is important to bear in mind that demand for traditional ICE models still far outweigh those for electric and it will remain so for some time. This gradual shift will be the defining challenge for all the traditional automobile brands.

Restructuring in The Automotive Industry

There has been pressure to restructure both from inside and out. Daimler acaba de anunciar seu plano de dividir sua divisão de caminhões comerciais do seu carro de passageiros um depois de ser pressionado pelos investidores para abalar o desconto do conglomerado correspondente e o valor de desbloqueio. Ele se tornará o mais recente em uma longa sequência de spin-offs semelhantes, com caminhões volu e parciais como Volvo por Volvo e Traton por Volkswagen. Dado o compartilhamento de muitas funções e marcas, haverá um desafio óbvio para manter estratégias de marca unificada. A marca, apesar de cair no estudo de financiamento da marca deste ano, que lutou no ano passado com um crescimento lucrativo à luz da epidemia, acaba de anunciar previsões de batedores de analistas e que parece se recuperar em 2022.

Mercedes-Benz, named for its key brand, will become the new face of the resulting passenger car company. The brand, although dropping in this year’s Brand Finance study as it struggled last year with profitable growth in the light of the epidemic, has just announced analyst-beating forecasts and looks likely to bounce back by 2022.

= Volkswagen, que também está olhando para a restrição, mas neste caso, interno. Ele deseja dobrar sua estratégia de várias marcas. Multipulares. Em vez de ser fiado, Porsche, juntamente com

There have been calls from some investors for the company to more formally spin-off both Porsche, Lamborghini, and other luxury marques to unlock value linked to Ferrari-like multiples.

However, the 84-year-old company is staying firm with its (at least for now) hallmark multi-brand strategy enabling it to pool investment costs – particularly around the shift to electric and hybrid powertrains – and insure against the reputational risk of the type seen following the diesel scandal. Rather than being spun off, Porsche, along with Audi, será um pilar central para essa estratégia.

Da mesma forma, Stellantis, anteriormente PSA e FCA, estão se preparando para os grandes investimentos necessário com a mudança do mecanismo de combustão interna. O acordo, sustentado por preocupações com a concorrência sobre o domínio do segmento de vans comerciais na Europa, acaba de criar a quarta maior empresa de carros do mundo com pressões potenciais para atualizar seu portfólio de marcas. 2035 (Escócia em 2032) e eliminar a gasolina e o diesel após 2040. Suécia, Islândia, Dinamarca e Holanda estão proibindo carros não elétricos a 2030. Noruega, onde os EVs atualmente compensam a metade de todas as vendas de carros e há mais de uma vez em que os dias.

Regulatory Pressure to Invest in Electric

Regulations all over the world, particularly in Europe, are pushing the industry towards electric cars.

The UK has announced it will ban sales of non-electric cars from 2035 (Scotland in 2032) and phase out petrol and diesel after 2040. Sweden, Iceland, Denmark, and the Netherlands are all banning non-electric cars by as early as 2030. Norway, where EVs currently make up around half of all new car sales and there are more Teslas per head than anywhere in the world is planning to ban new conventional car sales by as early as 2025.

A Alemanha está dobrando subsídios a veículos elétricos, removendo incentivos para carros de gelo e imposto sobre veículos em veículos elétricos até 2030 e investindo bilhões em infraestrutura de carregamento elétrico como parte de seu programa de ação climática 2030. A França tem um plano semelhante, se um pouco menos expansivo. Muitos estados individuais têm pacotes mais rígidos. A China, que está rapidamente se tornando o centro da geração de energia renovável e do mercado de veículos elétricos em todo o mundo, possui - semelhante ao Reino Unido - anunciou a eliminação de carros convencionais até 2035 e um pacote de incentivos para mover os fabricantes de carros para agir. A infraestrutura deve ser valiosa para o restante de sua vida útil e, ao mesmo tempo, as marcas precisam se preparar para o futuro. Mas o que vimos é que muitos grupos estão aumentando para o desafio:

The Federal US government is preparing an incentives package and President Biden has declared the whole government vehicle fleet will become US-made electric vehicles. Many individual states have stricter packages. China, which is fast becoming the centre of both the renewable energy generation and electric vehicle market worldwide, has – similar to the UK – announced the phasing out of conventional cars by 2035 and a package of incentives to move car makers to act.

Car Companies Responding With Massive Investment Plans

For brands this all presents a challenge.

From a production point of view, conventional vehicle production infrastructure must be made valuable for the rest of its useful life while at the same time brands need to prepare for the future. But what we have seen is that many groups are rising to the challenge:

nos próximos cinco anos, Volkswagen estará investindo € 73 bilhões em energia e digitalização de uma figura que é mais duplo para o seu período de 2015 e 2015. até 2025.

Leia nosso Entrevista com Klaus Zellmer, membro do conselho para vendas, marketing e pós -vendas na Volkswagen, onde ele nos diz mais sobre a iniciativa de sustentabilidade da empresa. 2040.

General Motors will have phased out all ICE vehicles by 2035 and become carbon neutral by 2040.

até 2025, Toyota espera ser 70% híbrido, 20% plug-in e apenas 10% de veículos de gelo. plug-hybrid. Até 2030, toda a frota será elétrica. No final de 2023.

Within five years, Ford is planning for all its European cars to be zero-emissions capable, all-electric, or plug-hybrid. By 2030, the whole fleet will be electric.

Hyundai is launching the IONIQ 5 in 2021 and plans to be selling over 500,000 EVs by 2025, aiming for a fully electric lineup in major markets by 2040.

Nissan, with its successful Leaf model, expects more than 1 million sales of electrified vehicles by the end of 2023.

, fica claro que em todas as regiões - embora com a Europa vendo uma mudança um pouco mais rápida - as montadoras estão enfrentando esse desafio com toda a sua energia combinada. Aumentando. O mesmo nível de confiabilidade do Ford ou VW? O mesmo nível de satisfação autoconfiante ao dirigir um Porsche?

Shift to Electric Changing the Brand Landscape

Given the incoming regulation, falls in ICE model resale value might push customers towards electric vehicles but as of right now resale prices actually seem to be increasing.

There therefore needs to exist a pull – both in terms of easing charging infrastructure concerns but also making electric models and brands high-functioning and aspirational.

Even when customers are in the category, how can brands convince customers that they will have the same level of safety as previously expected from a Volvo? The same level of reliability as for a Ford or a VW? The same level of self-confident satisfaction when driving a Porsche?

tudo isso levou a uma enxurrada de novas estratégias interessantes de marketing e marca. Vimos marcas completamente novas sendo criadas. A lista inclui novas marcas comerciais e acessíveis como Polestar, Lynk & Co a marcas de luxo e experimental ou de luxo como Faraday Future e Rimak. Volvo e

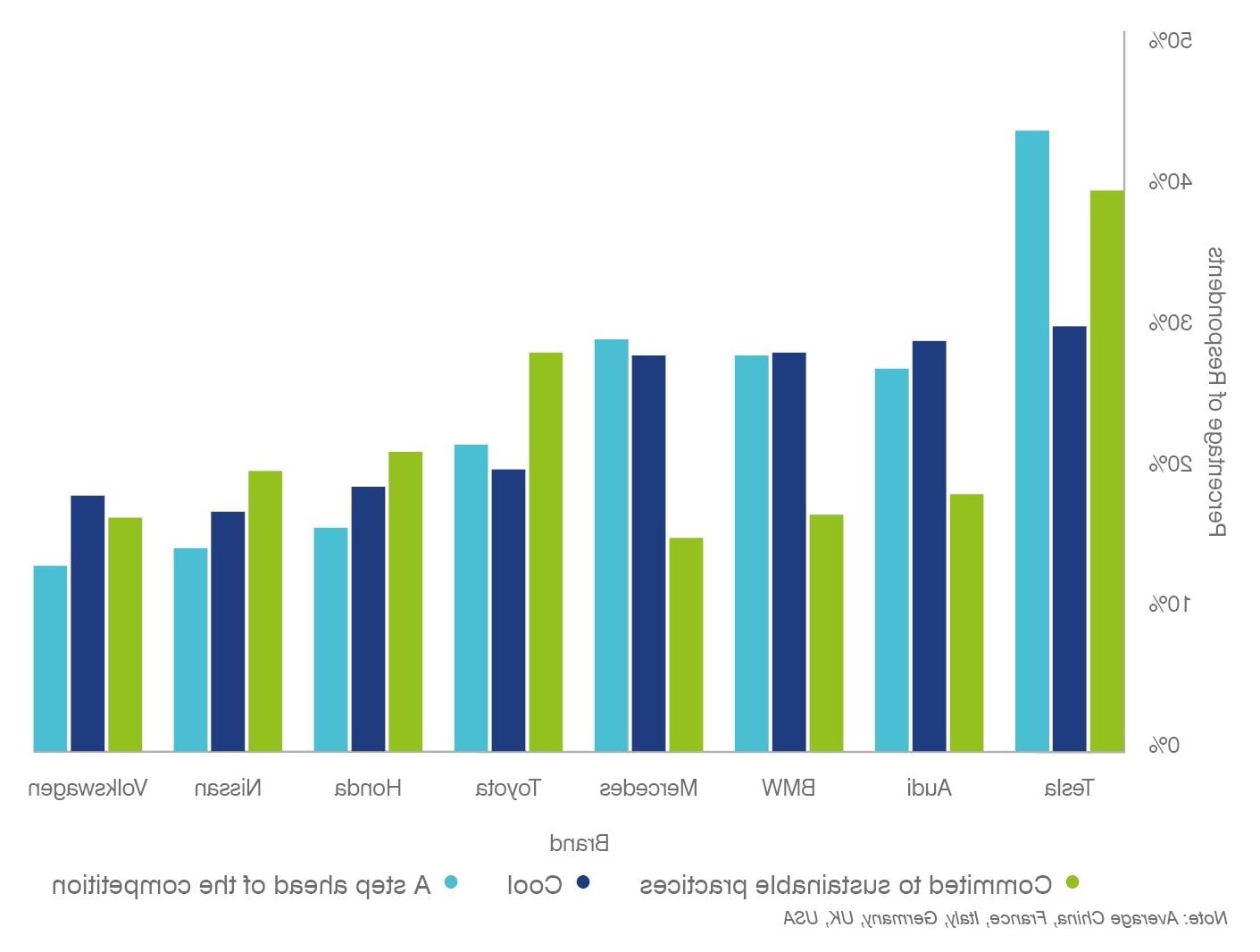

Many of these new brands are too small to make our table so, in reality, the most striking changes are those of existing brands. Volvo and Bentley Por exemplo, ambos anunciaram que estarão totalmente elétricos para a Volkswagen e BMW Anunciando e comercializando fortemente suas respectivas famílias "ID" e "IX" de novos modelos elétricos. O Volkswagen Group também anunciou a eletrificação de mais de 50 modelos existentes. Práticas sustentáveis e muito à frente em "Step Antes da competição", com quase 15% a mais pessoas dizendo que está à frente em comparação com a Mercedes, a próxima mais alta.

However, customers still need to be convinced that traditional ICE brands can walk the talk and Tesla still leads the pack on many attributes that could be key to the transition.

Looking at 8 of the most international brands, you can see that customers see it as more committed to sustainable practices and far ahead on “step ahead of the competition” with almost 15% more people saying it is ahead compared with Mercedes, the next highest.

É visto como mais "legal" do que qualquer outro 7 algo que será fundamental no segmento premium e mais do que se pode dizer de predecessores credenciados verdes como o Toyota Prius, sobre o qual houve muito mais discordância. Paridade de custo de alcance com carros de gelo até meados da década de 2020, talvez não seja surpreendente que eles sejam vistos como o pior valor pelo dinheiro de qualquer uma das 8 marcas selecionadas. Eles também são vistos como tendo a pior gama de produtos/modelos para escolher e seu atendimento ao cliente não é aquele que admira, com a Mercedes conquistando o primeiro lugar nessa importante medida por mais um ano. marcas. No entanto, no momento, o fator mais importante que ajuda as marcas tradicionais é o fato de serem muito mais conhecidas que a Tesla - apesar do hype. Depois disso, outros atributos desempenham um papel, mas se você não for conhecido, você é muito raramente considerado. Efetivamente, 30% a mais da população pode estar no mercado de Volkswagen do que poderia ser para Tesla. Surpreendente. A mudança de 2015 para 2019 é uma redução absoluta de 1,2%, equivalente a mais de uma redução total de 20% (dada as receitas crescentes) no investimento em marketing e vendas. Razões específicas da empresa para essas mudanças, mas a principal força de alguns dos jogadores existentes é sua importância entre os clientes impulsionados pela capacidade de investir amplamente no marketing. Marketing). Diferenças por mercado e detalhes a serem descobertos (particularmente em torno da inspeção final e da condução de teste), parece que as tendências, impulsionadas em parte pela pandemia covid, estão levando muitas marcas a um relacionamento mais direto ao consumidor. riscos. A curto prazo, o relacionamento com as concessionárias sofrerá. As vendas apenas a longo prazo, apenas on-line, não foram necessariamente gentis em mais mercados em estilo de commodities, como seguros e serviços públicos, embora a probabilidade de que isso aconteça com a indústria automobilística seja limitada. Perdê -los, portanto, exigiria um aumento nos gastos com marketing para compensar essa perda de exposição.

What is clear, however, is that Tesla is not dominant in everything and still has its issues.

Given the fact that electric cars are unlikely to reach cost parity with ICE cars until the mid-2020s, it is perhaps unsurprising that they are seen as the worst value for money of any of the selected 8 brands. They are also seen as having the worst range of products/models to choose from and their customer service is not one to look up to, with Mercedes taking the top spot on this important measure for another year.

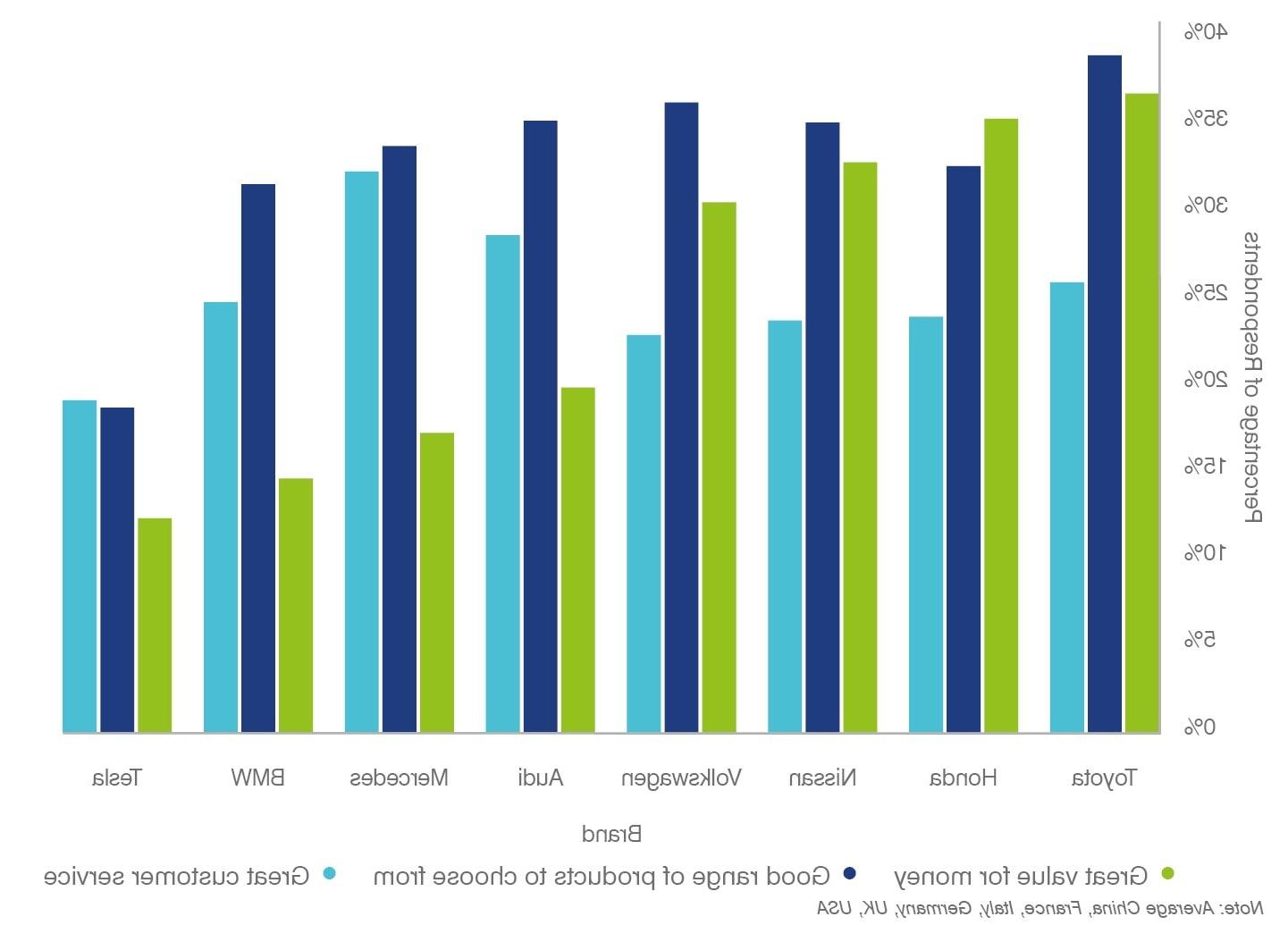

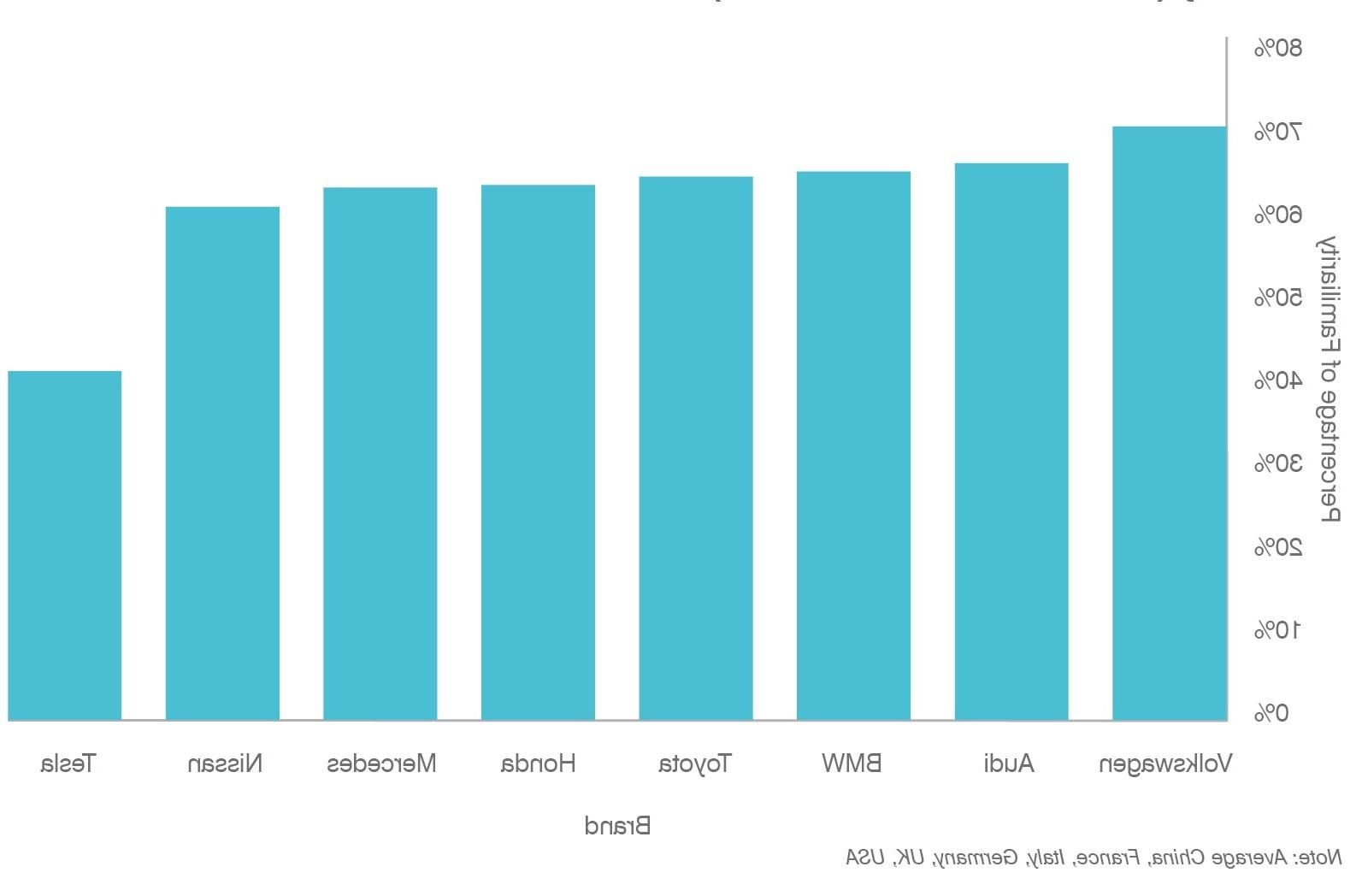

These measures are all important, and their importance should be analysed for each brand using positioning and drivers analysis in order to optimise the brand positioning and model response to Tesla and other electric car brands. However, right now, the most important factor helping traditional brands is the fact they are far better known than Tesla – despite the hype.

Familiarity and mental salience is the first building block in driving demand. After that other attributes play a part but if you are not known, you are very rarely considered.

Tesla has an average level of familiarity of only just over 40% while Volkswagen has a familiarity of over 70%. Effectively 30% more of the population could be in the market for Volkswagen than could be for Tesla.

This shows a clear limiting factor that can only truly be countered with marketing spend – a tool which the traditional OEMs have the money to invest in and the skill to activate effectively.

Marketing Spend Taking a Hit

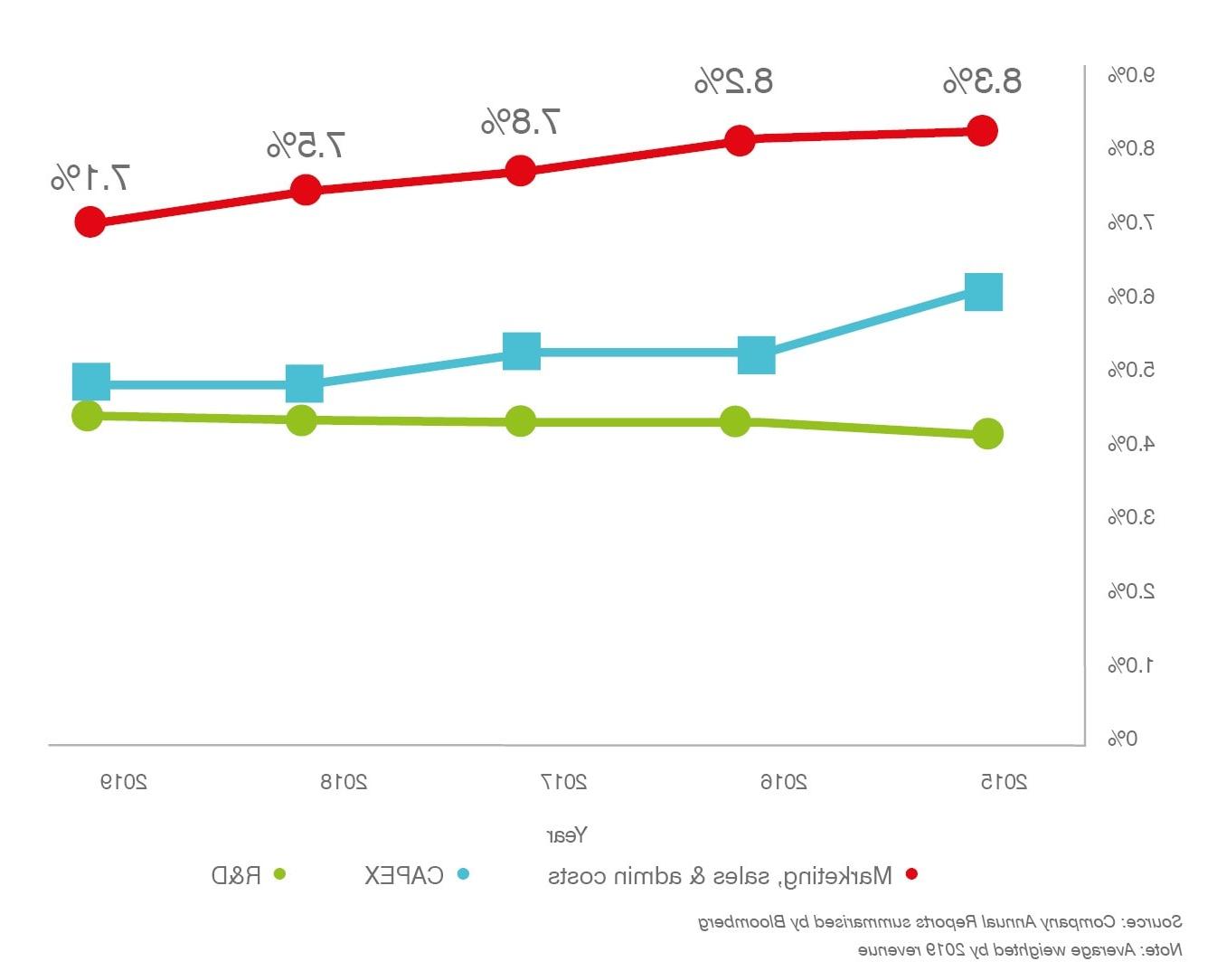

This is why recent pressures on marketing investment are surprising.

According to our analysis, marketing and sales investment fell steadily between 2015 and 2019 steadily and although most 2020 annual reports are yet to be published, anecdotally and from investor presentations we are aware marketing budgets have been pushed down even further. The shift from 2015 to 2019 is an absolute reduction of 1.2% which is equivalent to more than a 20% total reduction (given rising revenues) in marketing and sales investment.

CAPEX has also been dropping but given the need to depreciate existing production infrastructure this might make sense (especially given the newly announced plans for capital investment) but for marketing it is a less clear-cut story.

There are obvious company-specific reasons for these changes but the key strength of some of the existing players is their salience among customers driven by their ability to invest widely in marketing.

Cutting marketing investment can often be a fool’s game particularly given the ferocious competition driven by powerful, albeit cheap, word-of-mouth marketing for brands like Tesla (which itself will have to think soon about more traditional marketing).

New Approaches to Dealerships and Ownership

As of March 2021, as well as moving to fully electric, Volvo has announced that it will only sell its cars online by the end of the 2020s.

In a January 2021 study, Auto Trader identified that 41% of consumers would consider buying a car online.

Despite differences by market and details to figure out (particularly around final inspection and test driving), it seems that trends, driven partly by the COVID pandemic, are pushing many brands to a more direct to consumer relationship.

There are obvious benefits for OEMs to have this more direct relationship with data on buying patterns and the potential to capture margins from dealership being the most obvious.

However, there are clear risks. In the short-run, relationships with dealerships will suffer. Longer-term, online-only sales have not necessarily been kind on more commodity-style markets like insurance and utilities although the likelihood of this happening to the car industry is limited.

Dealerships also act as a useful out-of-home marketing media and purchase trigger. Losing them would therefore necessitate an increase in marketing spend to make up for this loss in exposure.

This move to online sales is also fuelling a new style of ownership, car subscription.

Este tipo de modelo de propriedade está em fase de crescimento rápido. As marcas Pure Play “Car-As-A-Service” estão sendo criadas e estão se consolidando como uma loucura. A Cazoo, uma das principais marcas nesta categoria, é uma varejista de carros on-line do Reino Unido que possui e recondiciona carros antes de vendê-los (ou permitir que os clientes se inscrevam) por meio de seu site com uma Política de devolução de uma semana completa. Reino Unido desde que foi lançado no ano passado. Por exemplo,

After buying UK-based subscription service Drover, it has recently announced it is buying Cluno in Germany and is growing very rapidly albeit from a relatively small base having delivered only just over 20,000 cars in the UK since it launched last year.

These new brands are rubbing up against brands in the traditional Car Rental industry. For example, HERTZ, Enterprise, Sixt==, || 378 and others are all moving in strongly.

This suggests that online sales could shake out as an online dealership model that adds efficiency for customers, produces price pressure at the lower end of the market, increases the role of brands in driving demand while potentially transferring some of the final elements of the customer experience to automobile brands. Much like the airline industry.

Em algumas circunstâncias, no entanto, as marcas de carros podem criar esse relacionamento direto. Porsche, por exemplo, está oferecendo à Porsche Drive, um modelo mensal de assinatura de carro com seguro e assistência na estrada incluía permitir que os clientes testem vários modelos da Porsche sem comprá -los. Dito isto, até que ponto isso pode sair do luxo ainda está para ser visto. Leia mais

We asked Porsche's CMO Robert Ader to tell us more about the company's electric transformation. Read more Aqui!

Embora a assinatura possa não ser a fonte de novos negócios para as marcas tradicionais, o leasing e a finanças do carro certamente é. De fato, a receita de financiamento agora representa uma média de quase 10% do valor da marca para as 10 marcas de automóveis mais valiosas este ano. Isso precisa ser refinado e definido à luz da mudança para os VEs. Os OEMs precisarão adotar essa categoria, reconhecendo que, à medida que os preços caem e a infraestrutura melhorar, a categoria se tornará o novo normal e essa categoria de clientes voltará à mistura original. (

What Does This All Mean for Auto Brands?

Car brands still create or enforce an identity for customers. This needs to be refined and defined in light of the shift to EVs.

During the shift to electric vehicles, there will be an overrepresentation of environmentally conscious, tech-savvy, urban, and wealthy customers interested in electric vehicles. OEMs will need to embrace this category while recognising that, as prices fall and infrastructure improves, the category will become the new normal and this category of customers will fall back into the original mix.

VW’s dual approach of offering electric models of its existing models while also launching an electric-only range recognises and exploits these different segments for example.

For some brands ( Ferrari, Harley-Davidson, Mustang, por exemplo), o desempenho e o som do motor é central para o posicionamento. Essas marcas precisarão identificar o período de tempo em que podem trocar esse posicionamento sem desaparecer lentamente na obscuridade ou como transferir atributos que funcionam em ambos os tipos de faixas de força - frieza, qualidade, serviço são todos essenciais em ambos, por exemplo.

Ferrari was named the world's strongest auto brand in our latest study. Saiba mais sobre a experiência da empresa através da pandemia global de seu diretor de comunicação, Jane Reeve. As principais razões para o driving range, a falta de infraestrutura de cobrança e o prêmio de custo envolvido.

Brands also still need to do convincing on the electric car category

Various surveys have found that many people are still reluctant to buy electric cars. The principal reasons being driving range, a lack of charging infrastructure and the cost premium involved.

As muitas novas inovações que estão sendo criadas para combater esses problemas precisam ser comunicadas mais amplamente. Serão necessários melhores showrooms on -line e geralmente mais foco na experiência de compra do cliente fora da concessionária. Já vimos turnos como grandes aumentos nos gastos com patrocínio dos OEMs e uma mudança para os canais de mídia digital - como em todos os grandes anunciantes.

Brands need to develop and decide how they will respond to the move online

There is an undeniable move to at least some of the purchase process being online. Better online showrooms and generally more focus on the customer buying experience outside of the dealership will be necessary.

Alongside these upgrades, a realignment of market budgets to recognise a shift in distribution channels and brand exposure. We have already seen shift such as been big rises in sponsorship spend by OEMs and a shift to digital media channels – as with all big advertisers.

No entanto, sem uma análise adequada do valor e retorno do investimento desses canais e a melhor maneira de ativá-los, sua eficácia pode ficar aquém. Dado o fato de a indústria estar mudando fundamentalmente, a medição da marca precisará combinar uma mistura de rastreamento de marca de período para periódio com a medição prospectiva de onde o valor vem no futuro e como garantir que esse valor seja maximizado. É provável que esteja no futuro. 2021

More forward-looking brand metrics

This need for better measurement extends beyond the need to analyse the effectiveness of channels. Given the fact the industry is changing fundamentally, brand measurement will need to combine a mixture of period-to-period brand tracking with forward-looking measurement of where value is coming from in the future and how to make sure that value is maximised.

Analysing brand strength using a scorecard, for example, looking at a mixture of investment attributes, brand equity, and customer equity can look further by using leading indicators to predict what brand perceptions are likely to be in the future.

Connecting them to brand value analysis helps to identify how that brand strength will impact business performance and therefore where to direct investment.

Combining this with existing, shorter-term measurements and hypotheses or plans for the future will help all OEM brands to add clarity in an industry where change is its principal characteristic.