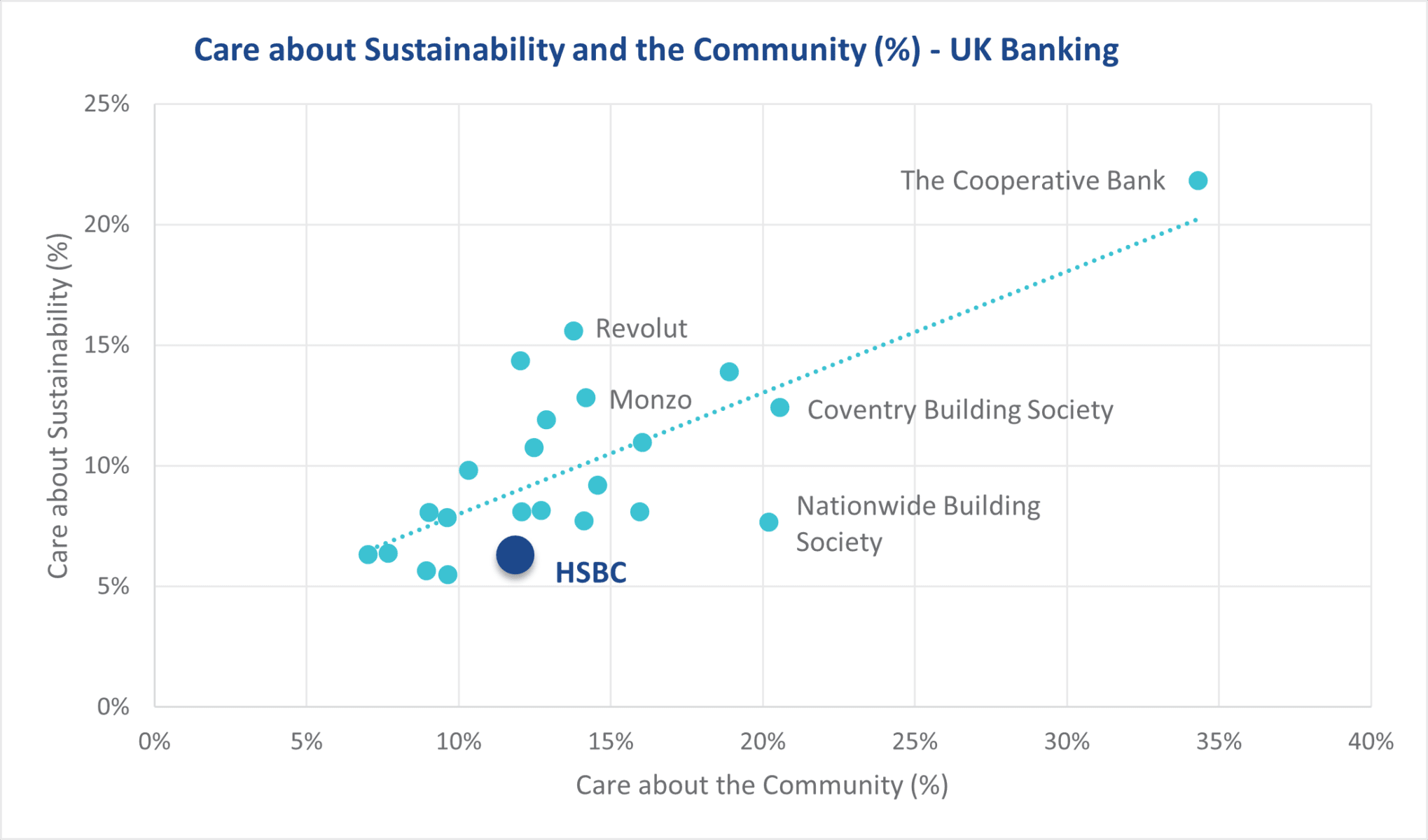

• As percepções verdes das marcas bancárias têm muito pouco efeito na aquisição de clientes entre os consumidores bancários de varejo. Autoridade de Padrões (ASA)-O cão de vigilância do Reino Unido, proibiu uma série de anúncios orientados para o clima pelo HSBC por enganar o público. Os anúncios foram centrados na mensagem: "A mudança climática não faz fronteiras, nem nós" em referência às metas de plantio de árvores do banco e zero de financiamento líquido. No entanto, o órgão de vigilância concluiu que os anúncios não divulgaram informações materiais sobre o financiamento de projetos do HSBC que muitos especialistas argumentam que contribuem para a crise climática. No entanto, podemos explorar por que o HSBC - e outros bancos do Reino Unido - optam por anunciar o tema de ser verde. A correlação entre como as marcas são classificadas para “se preocupar com a comunidade” e “se preocupar com a sustentabilidade”. Enquanto os bancos neo sem a pegada física e a bagagem histórica dos bancos tradicionais estão acima da indexação na métrica de sustentabilidade. O HSBC está com um desempenho ruim nas duas métricas. Isso contrasta com indústrias como automóveis, onde as emissões podem ser avaliadas diretamente pelo consumidor. No entanto, se olharmos para a reputação da marca por bancos do Reino Unido entre os consumidores do Reino Unido, vemos que os escores verdes estão correlacionados com a reputação geral:

• However, among small-to-medium sized businesses green perceptions are vital.

• Banking brands should focus on more important drivers of brand consideration to differentiate themselves in the market and improve customer acquisition.

A few days ago, the UK Advertising Standards Authority (ASA) – the UK advertising watchdog, banned a series of climate-orientated adverts by HSBC for misleading the public. The adverts were centred around the message, “climate change doesn’t do borders, neither do we” in reference to the bank’s tree planting and net zero financing goals. However, the watchdog concluded that the adverts failed to disclose material information regarding HSBC’s financing of projects that many experts argue contribute to the climate crisis.

Now, whether the adverts accurately portrayed reality, or indeed mislead the public is not for us to say. However, we can explore why HSBC - and other UK banks - are choosing to advertise around the theme of being green.

First, if we look at data from Brand Finance’s UK consumer banking survey, which includes 2 green metrics for banks:

Unsurprisingly there is a strong correlation between how brands are rated for “Caring about the Community” and “Caring about Sustainability.”

Interestingly, banks that position their offering around community (and not necessarily around being a traditional bank) such as The Cooperative Bank, Nationwide Building Society and Coventry Building Society are performing well in the community metric. Whereas Neo banks without the physical footprint and historic baggage of traditional banks are over indexing in the sustainability metric. HSBC is performing poorly in both metrics.

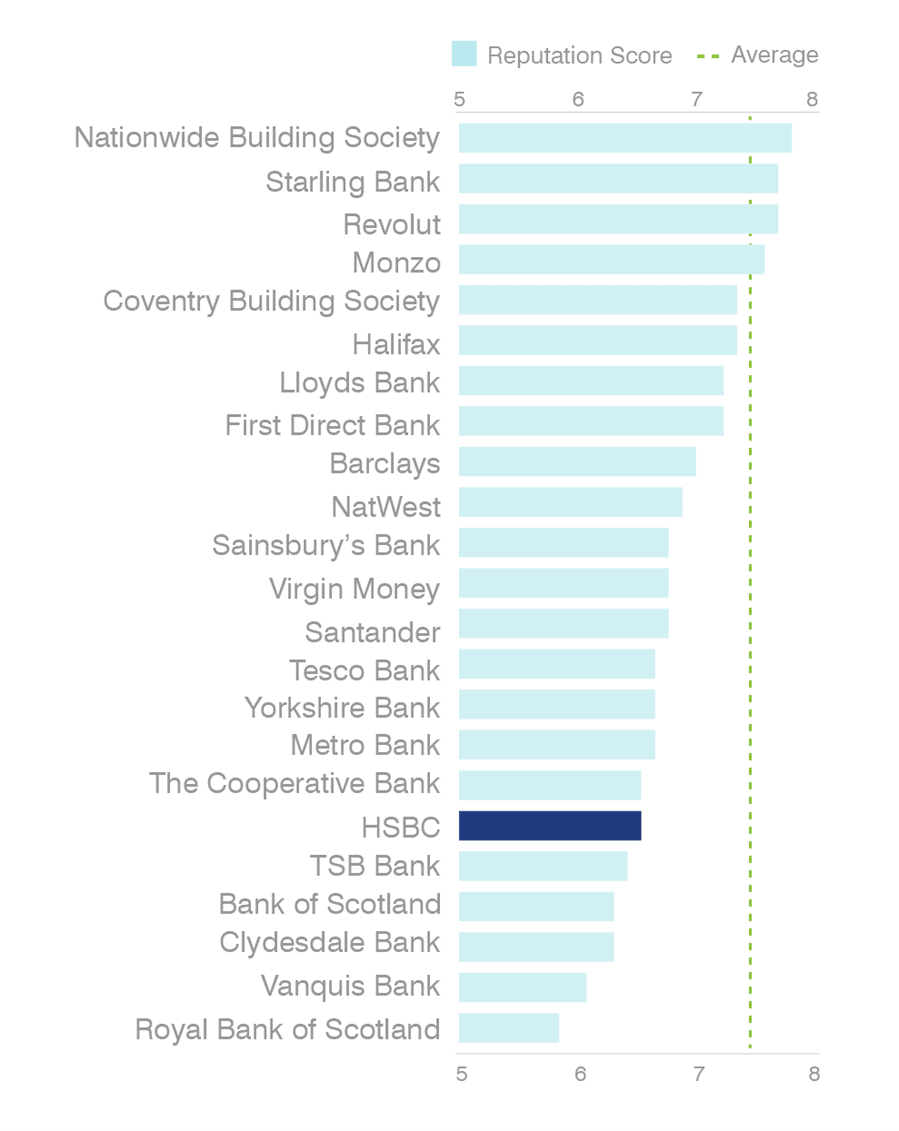

Some readers might look at the above data and think that it is not necessarily a significant issue that a bank scores poorly on certain green metrics given the nature of the services a bank provides. This contrasts with industries such as automobiles where emissions can be assessed directly by the consumer. However, if we look at Brand Reputation for UK banks among UK consumers, we see that green scores are correlated with overall reputation:

- Reputação - Reino Unido | B2B Banking

- Drivers of Brand Consideration - B2C banking

- What About Business Banking?

- Drivers of Brand Consideration – B2B Banking

- E a lucratividade dos bancos? Revolut, Monzo e Coventry Building Society têm as pontuações mais altas de reputação entre todas as marcas bancárias. Portanto, não é de surpreender que o HSBC esteja tentando corrigir a situação, executando campanhas publicitárias em torno do posicionamento verde (embora o fato de o banco cooperativo ter uma reputação relativamente ruim sugere que há algo além das percepções verdes que impulsionam as pontuações de reputação para essa marca). No entanto, é preciso fazer uma questão de mente mais comercial quando se trata de métricas verdes - os esforços verdes de uma marca bancária afetam a escolha do consumidor e impulsionam o desempenho dos negócios? É provável que o desempenho comercial do banco seja afetado porque possui baixas percepções do consumidor em torno da sustentabilidade e da comunidade?

Reputation – UK Banking

HSBC is languishing in 18th place with an average reputation score of 6.2, whereas the likes of Nationwide, Starling, Revolut, Monzo and Coventry Building Society have the highest reputation scores among all banking brands. Therefore, it is no surprise that HSBC is attempting to rectify the situation by running advertising campaigns around green positioning (Although, the fact that The Cooperative Bank has a relatively poor reputation suggests there is something other than green perceptions driving reputation scores for that brand).

Anecdotally, there appears to be a connection between green perceptions and reputation. However, one must pose a more commercially minded question when it comes to green metrics – does a banking brand’s green efforts impact consumer choice and drive business performance? Is the commercial performance of the bank likely to be affected because it has low consumer perceptions around sustainability and community?

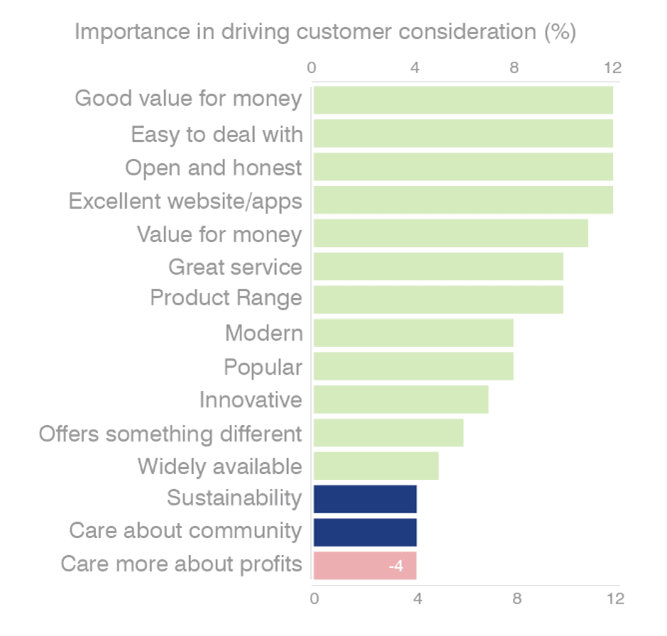

Para responder a essa pergunta, podemos mais uma vez examinar os dados. A execução de uma análise de regressão, normalmente conhecida como "drivers de marca", nos permite ver quais atributos da marca são os mais importantes para impulsionar a consideração do consumidor e, por extensão, aquisição do cliente.

Drivers of Brand Consideration - B2C banking

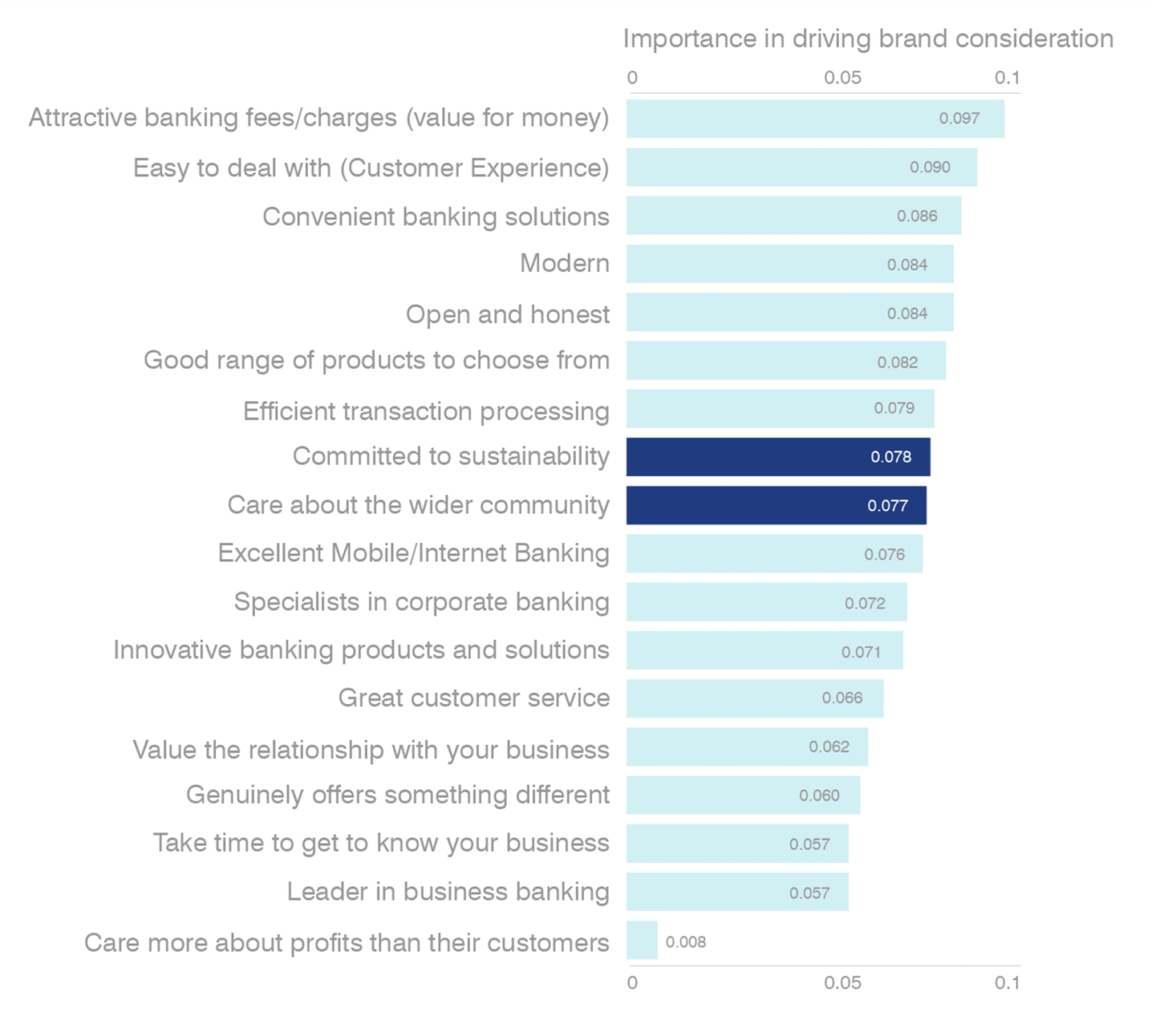

Given the role of banks in the Global Financial Crisis it is interesting that “open and honest” ranks third in attributes driving consumer choice, behind “good value for money,” and being “easy to deal with,” but ahead of having “excellent websites/apps” and “great serviço. ” “Sustentabilidade” e “Comunidade” são classificados em 2º e 3º último, respectivamente, quando se trata de correlação com a consideração da marca, apenas antes de “se preocupar mais com os lucros do que os clientes”, o que está negativamente correlacionado com a consideração. Isso então indica que o desempenho em métricas verdes não está necessariamente impulsionando os consumidores tomando decisões quando se trata de qual marca se basear. não tem um bom desempenho na comunidade e métricas sustentáveis. Mas essas métricas não são as mais importantes ao impulsionar a escolha do consumidor, independentemente de os consumidores insistirem que se importam muito com a "sustentabilidade". O que os dados indicam é que o HSBC tem um desempenho inferior para as métricas mais importantes aos olhos do consumidor: valor ao dinheiro, um serviço aberto e honesto, excelente serviço e excelentes sites e aplicativos. Está sob desempenho aqui que está levando a uma consideração e reputação mais baixas pelo HSBC entre os consumidores do Reino Unido. Quando o Push chegar a empurrar, um banco oferece melhores tarifas, serviços ou produtos geralmente ganham maior participação de mercado. Pode -se argumentar que muitas vezes há uma lacuna entre a importância declarada (ou derivada) e o comportamento real do consumidor. Felizmente, temos dados reais fornecidos pelo serviço de comutação em conta corrente no Reino Unido, que rastreou os ganhos da conta corrente líquida no mesmo período da pesquisa bancária da Brand Finance (outubro - dezembro de 2021):

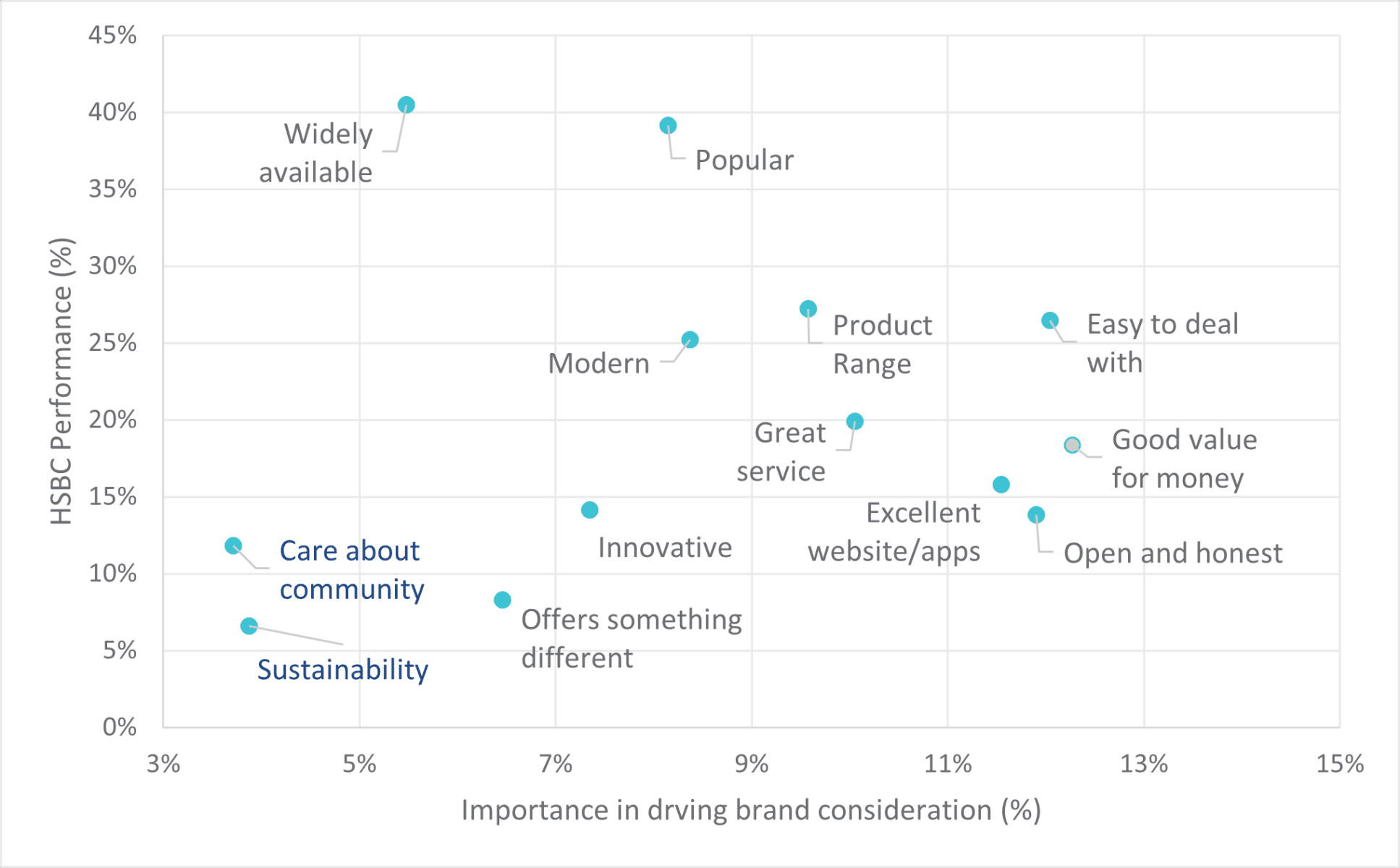

Finally, if we examine HSBC’s performance more extensively using an Importance vs Performance graph:

As mentioned earlier, HSBC does not perform well in the community and sustainably metrics. But those metrics are not the most important when driving consumer choice, regardless of whether consumers might insist they care very much about “sustainability”. What the data does indicate, is that HSBC underperforms for the most important metrics in the eyes of the consumer: value for money, open and honest, Great service, and excellent websites and apps. It is under performance here that is leading to lower consideration and reputation for HSBC among UK consumers.

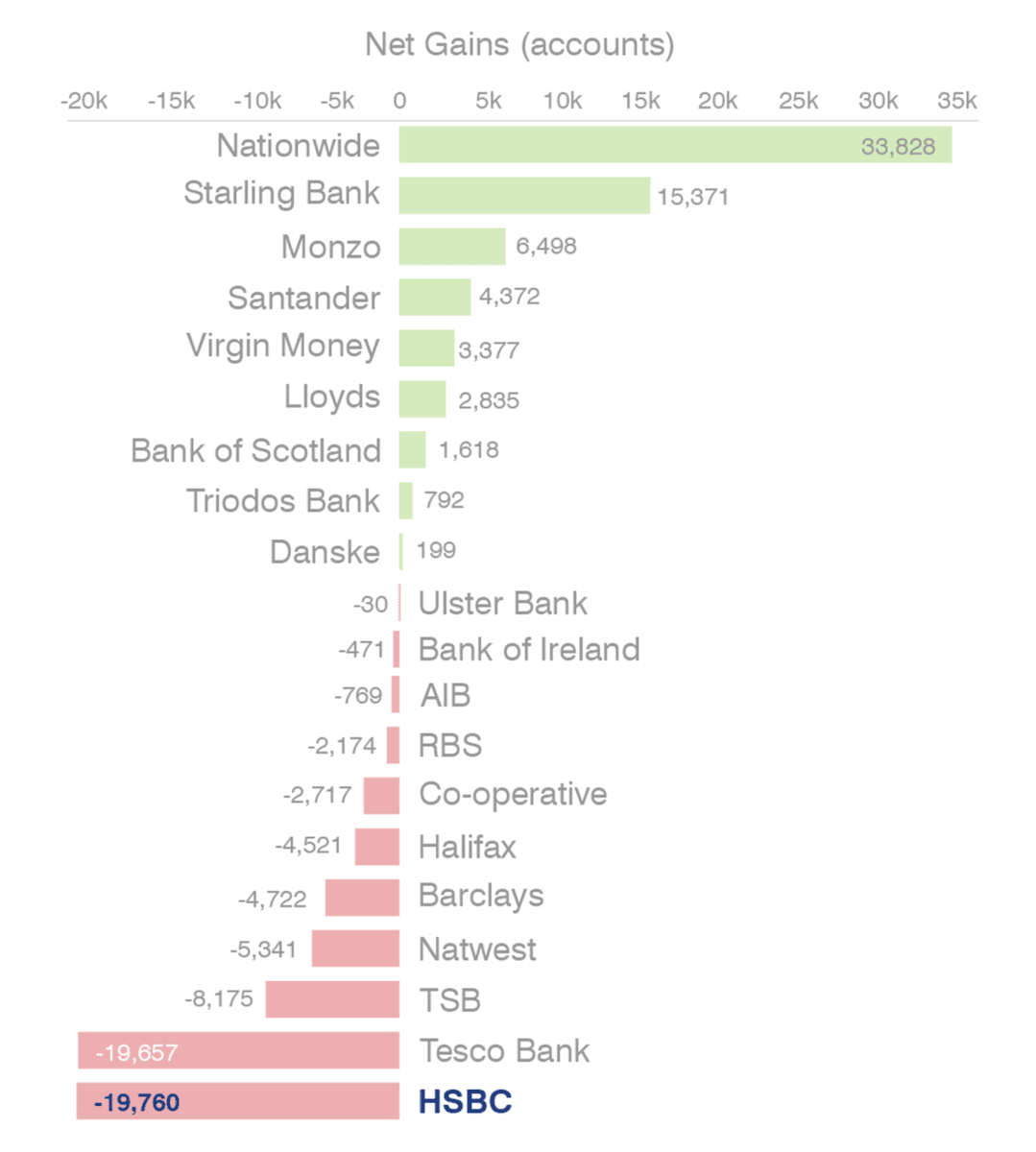

This data is a classic example of consumers stated good intentions to support causes like sustainability, being overtaken by more pragmatic concerns. When push comes to shove, a bank offering better rates, service or products will generally win greater market share. One may argue that there is often a gap between stated (or derived) importance and actual consumer behaviour. Fortunately, we have actual data supplied by the current account switching service in the UK, which tracked net current account gains over the same period of Brand Finance’s banking research (October – December 2021):

As you can see from the table, the brands the perform poorest in the derived importance metrics (HSBC) has the lowest net current account gain out of all participating banks. The banks the perform the best in the same attributes (and therefore have the highest brand consideration) – Nationwide, Starling, and Monzo, have the highest net current account gain.

What About Business Banking?

Many retail banking brands in the UK, HSBC included, have not yet worked out how to credibly differentiate themselves on sustainability. However, this does not mean they have not been trying. HSBC for example conducted an extensive worldwide study in 2021, with the firm Mintel, to uncover insights and deliver green banking products to consumers. HSBC say that the study led to new products being launched and future products being put into development.

One could argue that HSBC's recent adverts were focussed on the brand’s B2B services – highlighting for example how the bank had committed to investing $1 trillion in helping clients transition to Net-Zero. So perhaps green positioning is important in the B2B space?

Drivers of Brand Consideration – B2B Banking

According to research conducted by Brand Finance (and supported by further qualitative research) B2B customers are much more concerned about a banking brand’s credibility in green metrics. The B2B space perhaps provides more credible ways a brand can demonstrate green credentials (funding of green projects or underwriting green bonds for example) than in the consumer space, which is why we see greater importance placed on green metrics among B2B customers. There are other stakeholders for the business of course, which should not be ignored. Attracting and retaining good talent and adhering to the requirements of the investor community are all reasons to take part in sustainable projects and market your credentials.

However, perhaps more focus should be placed on the green credentials of the actual products and the banks in question, rather than those of the bank’s customers. For example, many banking brands continuously refer to net-zero financing goals or the issuance of green bonds, but this is aimed at the activities of the project being funded or of the specific client in question, and not at the green credentials of the bank themselves.

e a lucratividade dos bancos?

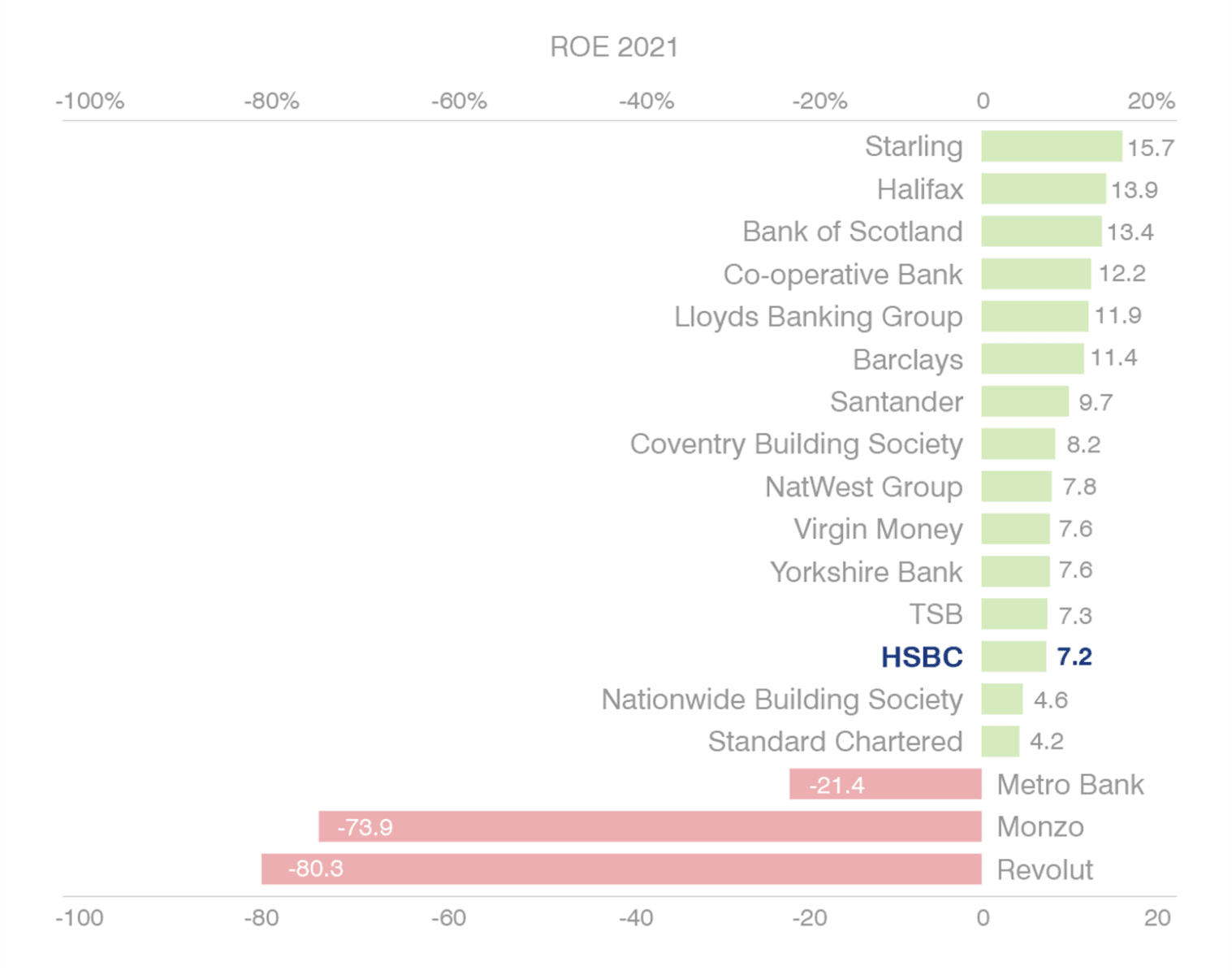

Finalmente, o verdadeiro fator motivador para um banco sobre se deve seguir práticas sustentáveis ou não é certamente impulsionado pelos lucros. Se olharmos para o retorno do patrimônio (ROE) dos bancos do Reino Unido no ano fiscal de 2021:

A lucratividade parece indicar resultados mistos quando se trata de percepções de sustentabilidade. Por exemplo, o HSBC é mais lucrativo que em todo o país - apesar de em todo o país ter a melhor reputação no mercado, bem como as mais altas aquisições de contas líquidas. Enquanto os gostos como Starling, Halifax e Banco Cooperativo são altamente respeitáveis e altamente lucrativos. É improvável que o próprio HSBC esteja preocupado demais com o volume de contas que se afastam do banco, pois a hipótese aqui é que esses são clientes de muito baixo valor, com baixos depósitos e necessidades bancárias sem complicações (e, portanto, não são uma prioridade para eles). Esses resultados defendem por que a importância da forte governança e regulamentação é necessária para impor boas práticas de sustentabilidade no setor bancário do Reino Unido. Pouca defesa emocional e a marca estão alavancando o poder da boa publicidade, mas não há pontos de prova racional suficientes e uma marca pode ser vista como inautêntica pelo cliente (para não mencionar outras partes interessadas). O que a análise acima confirma é que existe uma oportunidade para todas as marcas bancárias no espaço B2C e B2B para mostrarem suas credenciais de credibilidade no espaço verde e diferenciar seus produtos e serviços de suas marcas daqueles de seus concorrentes. um analista. Durante seu tempo na empresa, ele progrediu para seu cargo atual como diretor de avaliações da Brand Finance Plc e diretor de Financeiros da Brand Africa. Declan lidera a equipe que produz o estudo anual mais valioso das marcas bancárias globais em colaboração com a revista Banker (o FT). Ele escreveu e contribuiu para vários trabalhos de liderança e acadêmico do pensamento da indústria e é orador regular de várias conferências, como a conferência Rising da IAA Africa. Os clientes de Declan incluem absa, Banco de Access, Citi Bank, TD Bank, First National Bank, Royal Bank of Canada, QNB, entre outros. Economia. FINANCE

Ultimately, brand-building needs to focus at the intersection of emotional advocacy and rational proof points. Too little emotional advocacy and the brand is under leveraging the power of good advertising, but not enough rational proof points and a brand might be viewed as inauthentic by the customer (not to mention other key stakeholders). What the above analysis does confirm is that there is an opportunity for all banking brands in both the B2C and B2B space to credibly show their credentials in the green space and differentiate their brands products and services from those of their competitors.