Este artigo foi publicado originalmente no Indústria automotiva de finanças da marca 2022 Relatório. significativo

2022 Automotive Industry Trends: Doubling Down on Electric and Connected Cars

- All sub-sectors within the industry are rebounding from the pandemic

- Demand is growing but the costs of transition to EV are significant

- Apesar das marcas OEM que precisam atualizar cuidadosamente seu posicionamento para a revolução EV, os gastos com marketing estão caindo

- As vendas on -line continuam a oferecer uma rota para melhorar a experiência da marca

- Resumo Scorecards da carteira precisava mais do que nunca || 107

- What has been happening to the industry?

- 2021/22: recuperando-se da pandemia

- Mobilidade multimedium

- Aceleração de veículos elétricos

- ROAD CURQUIRA, FECTATIONA & ZERO EMISSIONSIONES DESIVERTA EM INFOTIFICATRANTIATRATULATIONATRATIVA, ROTATILOMIATROTILOMIATROTIVOS EM INFOTIVAS DO ROTOMENTO EM INFOVERTA EM INFOTIFICAÇÃO DO ROTO, AUTOMOMS ||hisions emissões de frete e zero. Marketing)

- Connectivity & Autonomous Vehicles

- Focus of Investment Changing (R&D versus Marketing)

- Mudança de foco para as marcas de componentes automáticos

- Mobilidade como um retorno de serviços de aluguel e serviços de carro

- concessionárias de carros, vendas on -line e novas marcas de carros usados

- SO que significa para as marcas? | Para ver grandes mudanças nos modelos de negócios, à medida que o ritmo da eletrificação aumenta e os avanços na tecnologia de conectividade continuam. O impressionante crescimento de marcas lançadas recentemente. Esses novos iniciantes estão aumentando a classificação em termos de valor, enquanto as marcas mais estabelecidas tiveram um crescimento mais moderado. aumentando. A inovação continua em um ritmo forte, o investimento em nova capacidade, principalmente para veículos elétricos (VEs), está aumentando, e a demanda dos clientes está aumentando. Apesar das pressões, as perspectivas para a indústria são positivas. O crescimento da economia e das taxas de juros relativamente baixas aumentou a demanda por todos os tipos de mercadorias-os carros incluídos. Os lucros também aumentaram, em média, nos OEMs este ano, com muitos fazendo números recordes. Isso é, em certa medida, corroer as diferenças anteriormente grandes na popularidade do tipo de modelo entre as regiões - como a tendência européia para carros pequenos e os EUA para modelos maiores. Em 2021, foram vendidos cerca de 6,4 milhões de veículos elétricos - um aumento de mais de 100%. Isso representa um aumento de 4,5% de todos os veículos vendidos em 2020 a 9% em 2021.

What has been happening to the industry?

As 2022 begins, the automotive industry is continuing to see huge changes in business models as the pace of electrification rises and advances in connectivity technology continue.

These changes are giving rise to intense competition that is undermining existing brand strategies, and have given rise to huge new opportunities for both existing Original Equipment Manufacturers (OEM) and new brands alike.

The changing landscape is evidenced by seven new entrants in the Top 100 this year, compared to only two last year, and the impressive growth from recently launched brands. These new starters are racing up the ranking in terms of value, while more established brands have seen more subdued growth.

The combined pressures of evolving mobility, changing drivetrain and model type requirements, a shifting customer and regulatory landscape, and new technology requirements are all creating an inflexion point for the industry, and the brands within it.

However, the industry has shown resilience with both sales and values increasing. Innovation is continuing at a strong pace, investment in new capacity, particularly for electric vehicles (EVs), is soaring, and customer demand is increasing. Despite the pressures, the outlook for the industry is positive.

2021/22: Recovering from the pandemic

Overall, the automotive industry is recovering from the effects of the pandemic. Growth in savings as well as sustained relatively low interest rates have pushed up demand for all types of goods – cars included.

As a result, according to Euromonitor, unit sales volumes in 2022 are expected to be around 78 million units (+10% on 2021, which is itself up 10% on 2020), beating the pre-pandemic 2019 levels. Profits also rose on average across OEMs this year, with many making record numbers.

SUVs and SUV crossovers remain the most popular models, and that popularity continues to grow in all regions. This is, to some extent, eroding the previously large differences in model type popularity between regions – such as the European tendency for small cars and the US one for larger models.

Although demand looks positive across the industry, EVs are by the far the best performing drivetrain type in terms of relative growth. In 2021, about 6.4 million plug in electric vehicles were sold – an increase of over 100%. This represents a rise from 4.5% of all vehicles sold in 2020 to 9% in 2021.

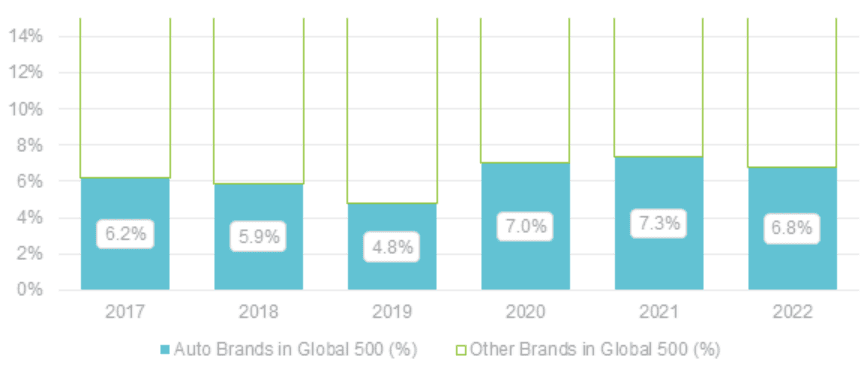

O principal obstáculo que mantém os OEMs de volta é o acesso a microchips, que se prevê permanecer um problema por algum tempo. Além disso, outro grande obstáculo para o crescimento do valor é o efeito no sentimento dos investidores das grandes mudanças que ondula pela indústria. Este ano, observamos aumentos razoavelmente grandes no sentimento de risco para a indústria, o que aumenta os custos de financiamento e reduz os valores em geral.

parcialmente como resultado desse risco adicional, a proporção de valor da marca automobilística no ranking Global 500 da Finance Brand Global caiu pela primeira vez em 3 anos, de 7,3% para 6,8% do total. O valor absoluto das marcas de automóveis na Finances de marca Global 500 A classificação realmente aumentou 5 %, mas aumentos mais fortes no crescimento para os setores de varejo, tecnologia, mídia e viagens de uma marca de marca de automóveis. respectable 4.3% increase overall – with the total brand value growing from US$5.9 billion in 2021 to US$6.1 billion in 2022.

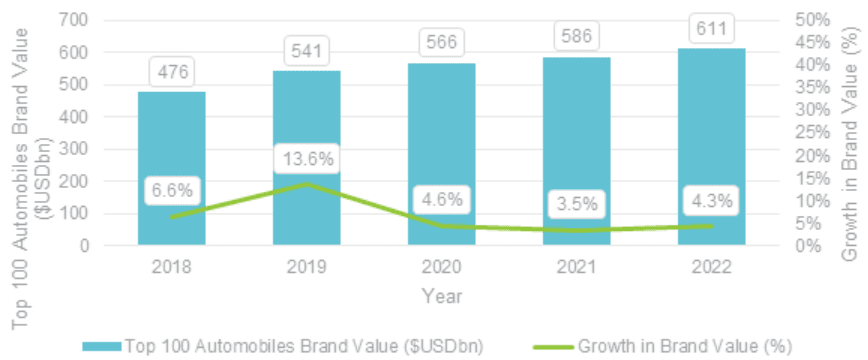

Looking back to Brand Finance Automobiles 100 ranking, the brands featured registered a respectable 4.3% increase overall – with the total brand value growing from US$5.9 billion in 2021 to US$6.1 billion in 2022.

This growth was across the board, but particular focus needs to go to China which is home to eight of the Top 10 fastest-growing brands, and 7% of the total brand value in the ranking, up from 5% in 2021. As marcas chinesas aproveitaram com sucesso o esforço de VEs na China e agora estão se movendo em todo o mundo. de multimédio e micro-mobilidade e as reações relacionadas contra carros por muitas cidades, especialmente em partes mais ricas do mundo.

These results show an industry adapting to a period of a significant strategic challenge and high investment requirements, shaking up old players and introducing new ones rather successfully.

Multi-medium mobility

Looking forward, there are significant threats to the industry’s continued strength, – in particular, the rise of multi-medium and micro-mobility and the related reactions against cars by many cities, especially in more affluent parts of the world.

Um estudo recente da McKinsey mostra que até quatro quintos de pessoas estão dispostos a usar bicicletas, ciclistas ou scooters para se deslocar para o trabalho. Lime, VOI e muitas outras empresas de scooters estão atingindo uma escala significativa, enviando IPOs e tendo sucesso comercial relativamente forte como provedores de serviços de mobilidade alternativos. Na última contagem, mais de 150 cidades da Europa introduziram regulamentos para favorecer carros de baixa emissões em relação aos modelos tradicionais de gelo e a mesma tendência está sendo vista em menor grau em todo o mundo. Embora um pouco mais de desconto no tempo, a mobilidade do ar pessoal também sofreu um enorme aumento no investimento nos últimos dois anos. Combinado. O primeiro deles, em Coventry, estará operacional no início de abril deste ano. Os efeitos combinados das opções de micro-mobilidade (curta distância) e mobilidade de ar personalizada (longa distância) provavelmente causará pressão significativa nos OEMs automotivos tradicionais no futuro. Finanças Automobiles 100 2022 Classificação. A Tesla continua seu crescimento - aumentando 40%, para US $ 46,0 bilhões e levantando três fileiras para se tornar o 3

Paris, Berlin, Barcelona and many other cities are making life more difficult for cars – especially those with an internal combustion engine (ICE). At last count, over 150 cities in Europe had introduced regulations to favour low emissions cars over traditional ICE models and the same trend is being seen to a lesser extent across the world.

These close-distance mobility trends are also not the only way our modes of mobility might change in the near future. Although a little further off in time, personal air mobility has also seen a huge increase in investment in the past two years.

According to S&P Global Intelligence, the total value of venture capital investment, together with associated R&D spending and announced SPAC mergers in personalised air mobility, was almost four times higher in 2020 and 2021 (at ~$9.8bn) than it had been in all years up to 2019 combined.

UK start-up, Urban-Air Port, has announced plans to build 200 “vertiports” for vertical take-off and landing of cargo drones in addition to launching passenger craft in 65 cities globally, in collaboration with Hyundai. The first of these, in Coventry, will be operational as early as April of this year.

According to some estimates, these advanced air mobility options could account for over 50% of long-distance journeys within the next 20 years – especially in cities and regions with high levels of road congestion. The combined effects of micro-mobility options (short-distance) and personalised air mobility (long-distance) is likely to cause significant pressure on traditional automotive OEMs in the future.

Electric Vehicles' Acceleration

Despite these headwinds, there is a huge opportunity in electric vehicles that most of the OEMs are seizing strongly.

EV brands are the big success stories of the Brand Finance Automobiles 100 2022 ranking. Tesla continues its growth – increasing by 40% to US$46.0 billion and raising three ranks to become the 3 RD Marca de automóveis mais valiosos. Ele não apenas manteve com sucesso sua capacidade de produção e superior em termos de vendas de modelos de EV, mas também armazenou valor em termos de futuras receitas de software em cativeiro. - Comece a internacionalizar. Nio, Airways, BYD, Dongfeng Motor, SAIC e Great Wall, nossa marca que mais cresce, todos lançados na Europa no ano passado.

Nio, Tesla’s Chinese competitor, has grown 79% following a boom for EV sales in China this year, which have increased by 150% in 2021 and look likely to double again in 2022. However, it is not only China fuelling this rise as Chinese brands – especially EV brands – start to internationalise. Nio, Airways, BYD, Dongfeng Motor, SAIC, and Great Wall, our fastest-growing brand, all launched in Europe last year.

A mudança para os VEs beneficiou extremamente as marcas chinesas. Com a tecnologia de gelo, a China estava jogando apanhação, mas no espaço EV, muitas marcas chinesas estão na vanguarda. Não apenas essas baterias serão usadas para carros BYD, mas também a marca está em negociações para fornecer baterias da Tesla e criou uma joint venture com a Toyota. Pode-se razoavelmente imaginar isso acontecendo com os EVs chineses, e especialmente BYD: uma versão chinesa de “Vorsprung Durch Technik”, talvez?

For instance, BYD unveiled its “Blade Battery” in the second half of last year, which holds 50% more electricity than similar battery chemistries, is safer when damaged, and avoids the controversial metals cobalt and nickel. Not only will these batteries be used for BYD cars, but also the brand has been in talks to supply Tesla with batteries, and has created a joint venture with Toyota.

Many of the German brands built their marques on the strength of their engines and the associated engineering. One could reasonably imagine this happening with Chinese EVs, and especially BYD: a Chinese version of “Vorsprung durch Technik” perhaps?

Marcas tradicionais estão se recuperando. Todos os principais OEMs têm planos de investimento de vários bilhões de dólares para eletrificar suas faixas, e você pode vê-los repetidamente apressar as declarações para os concorrentes da One-Up-por exemplo, o compromisso da Volkswagen em dezembro de 2021 de aumentar o investimento em € 17 bilhões para € 52 bilhões, o maior investimento de qualquer manufatura. À medida que os países introduzem os requisitos de qualidade e emissões do ar cada vez mais atrevidos, os OEMs investem muito mais e os VEs se tornam dominantes, a marca e as mensagens em torno de novos carros de EV perderão alguma distinção sobre suas credenciais verdes. Um trem de força sustentável não será mais um diferenciador. Isso exigirá o uso de componentes reciclados, mudando para matérias -primas verdes e evitando insumos controversos que às vezes são usados na fabricação de baterias. A nova marca de Luxury EV da Polestar, que ainda precisa entrar em nossa mesa, descreve algumas maneiras ousadas de fazer isso, mantendo o apelo de luxo em seus novos carros conceituais. Familiarizados com uma marca que afirma que é "sustentável"

This raises an important point about positioning as car brands move electric. As countries introduce ever-stricter air quality and emissions requirements, OEMs invest much more, and EVs become dominant, branding and messaging around new EV cars will lose some distinctiveness over their green credentials. A sustainable powertrain will no longer be a differentiator.

The sustainability of the production process for EVs – which some estimates say creates 80% higher production emissions than ICE vehicles – will be a point of difference. This will require using recycled components, shifting to green raw materials, and avoiding controversial inputs that are sometimes used in battery manufacturing. Polestar, Volvo’s new luxury EV marque, which has yet to break into our table, outlines some bold ways to do this while maintaining luxury appeal in its new concept cars.

This is proving helpful for Volvo’s positioning in the area of sustainability, but for BYD and Tesla, brands more closely associated with EVs, sustainability is a much clearer differentiator.

Igualmente, conforto e conectividade, juntamente com recursos mais básicos, como alcance e confiabilidade, se tornarão essenciais. Você pode ver com a prevalência de sub-marcas baseadas em tecnologia-BMW I, Volkswagen ID, Audi E-Tron etc-que muitas marcas estão empregando a tecnologia para ser a base de seu posicionamento. Baseando um posicionamento em torno de investimento contínuo e tecnologia de ponta quando você não a possui, é improvável que seja um jogo vencedor. "Inovador"

BMW, which is the most reluctant of the big German OEMs to invest in the EV transition, has also been one of the slowest growing brands in the ranking. Basing a positioning around continuing investment and cutting-edge technology when you don’t have it, is unlikely to be a winning game.

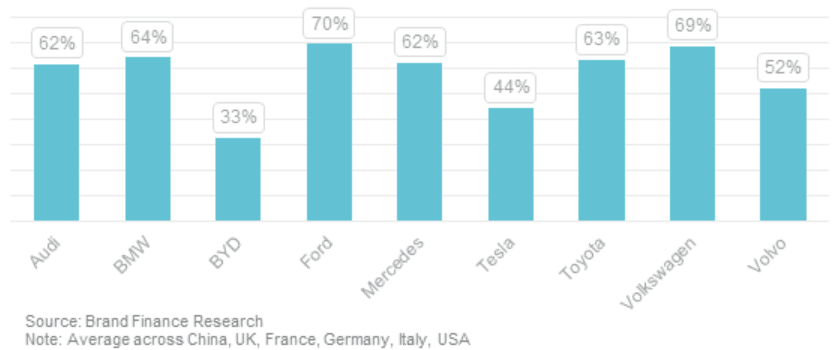

That being said, the premium German OEMs are all still considered highly innovative, with over 30% of customers familiar with the brands agreeing they are innovative, so for the time being this positioning focus seems to be possible and positive for the brands.

Apesar do surgimento de novas marcas elétricas, é provável que as marcas tradicionais permaneçam no topo, desde que façam os investimentos apropriados na transição do EV. Nossa pesquisa mostra que a familiaridade da marca - a chave para manter a participação de mercado - ainda está bem à frente das marcas tradicionais e sua reputação de qualidade e inovação estão intactas. Se as tendências na micromobilidade se mantiverem nas cidades, o crescimento de longo prazo dos VEs dependerá de popularidade ampla em regiões pesadas de carros, particularmente em áreas rurais e suburbanas. Nessas áreas, a aceitação social e as credenciais verdes podem ser úteis, mas o desempenho, a confiabilidade e o desfrute de pilotagem também serão fundamentais. Europa, mas há sinais de rebote em todo o mundo.

One final point to consider is that EV model popularity has predominantly taken root in environmentally conscious regions and cities. If the trends in micromobility do take hold in cities, EVs’ long-term growth will be dependent on broad-based popularity in car-heavy regions, particularly in rural and suburban areas. In these areas, social acceptance and green credentials may be useful, but performance, reliability, and riding enjoyment will also all be key.

Road Trucks, Freight & Zero Emissions Vehicles

Road freight had a reasonably strong year – for the 12 months up to October 2021, road freight in Europe was 8.3% higher than the equivalent period up to October 2020. his has not reached pre-pandemic levels in Europe, but there are signs of a rebound across the world.

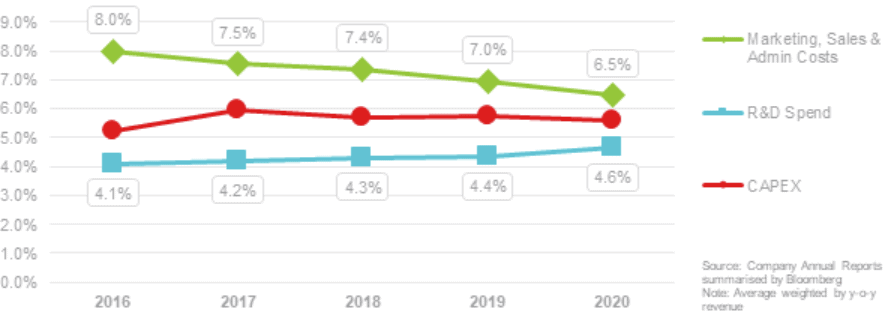

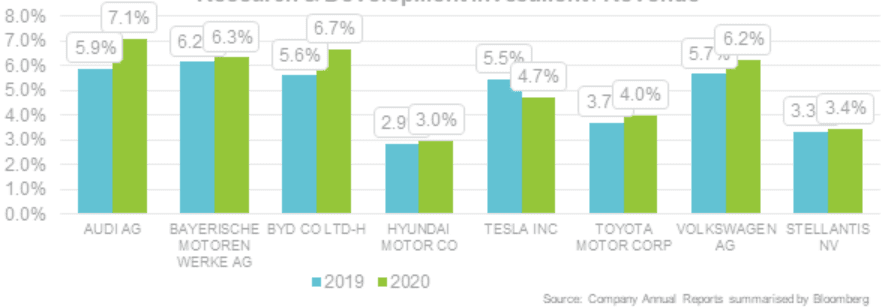

Os valores de marcas de caminhões tiveram um resultado igualmente misto este ano, com sinais razoavelmente fracos de uma recuperação, mas, no entanto, sinais. Scania, caminhões Volvo e caminhões UD todos registraram pequenos aumentos no valor da marca, mas, inversamente, o homem registrou uma queda de 18% no valor da marca para US $ 2,2 bilhões. Tanto a tecnologia de hidrogênio quanto a tecnologia de bateria elétrica será necessária, e o investimento precisará ser significativo, uma vez que apenas 5% dos caminhões na Europa-que estão na vanguarda da redução de emissões-atualmente são emissões zero. Traton-o proprietário do homem e da scania-está lutando sob os requisitos de investimento, mas resultados recentes sugerem que a recompensa pode estar à vista. Vantagem em primeiro lugar para marcas de caminhões premium, como a Scania, para fornecer caminhões em emissões zero a preços premium, mas os custos precisarão cair na adoção generalizada e-como nos carros de passageiros-os diferenciais para as marcas mudam para a tecnologia de gentileza. Embora os EVs atualmente não tenham uma vantagem significativa, muitos acreditam que, no futuro, os EVs terão uma milhagem maior ao longo da vida, duram mais e melhor retendo seu valor. Indústrias, complementos e assinaturas de software baseados em tecnologia provavelmente se tornarão uma parte significativamente mais importante dos modelos de negócios. A Tesla, por exemplo, cobra US $ 10.000 por seu complemento "Autocrodução", que seu CEO, Elon Musk, disse que poderia finalmente atingir um valor de US $ 100.000-mais do que o valor do carro original-e ser espalhado pela vida do carro em um modelo de assinatura. O potencial de valor desse tipo de inovação é claro, mas os requisitos de investimento e inovação serão significativos. Cada vez mais, está ficando claro que o caminho para a condução autônomo envolverá pequenos incrementos, em vez de investimentos na lua como os do Uber, Google e Apple - que ainda estão muito longe de ter um caso de negócios sólido. de conectividade também pode ser um motivo para questionar a ascensão de marcas chinesas fora da China. Dado o nível de coleta de dados exigido e a importância da confiança no software, alguns consumidores fora da China podem relutar em comprar marcas chinesas, dado o estado das relações entre a China e o Ocidente. Recentemente, no entanto, o CAPEX tem sido estável como uma proporção de receita. O investimento em P&D aumentou modestamente com um crescimento relativamente alto no ano passado e agora é equivalente a 4,6% da receita para marcas de automóveis listadas. Isso é equivalente a um aumento absoluto de US $ 700 milhões entre 2019 e 2020 (crescimento de 0,6% em comparação com 2019). Esses aumentos são sinais positivos, mas serão necessários mais para aproveitar as oportunidades que o setor está enfrentando. Além do que a Tesla de rápido crescimento gasta. Audi, BMW e Volkswagen aumentaram os gastos em P&D como uma proporção de receita no ano passado e têm uma taxa média de investimento de 6,6% - maior que a média do setor.

This is because, despite the increases in demand, the spectre of the zero-emissions transition hangs heavy over the industry. Both hydrogen fuel-cell and electric battery technology will be necessary, and the investment will need to be significant given that only 5% of trucks in Europe – which is at the forefront of emission reduction – are currently zero emissions. Traton – the owner of MAN and Scania – is struggling under the investment requirements, but recent results suggest the payoff could be in sight.

Many of the same issues that affect passenger car brands affect trucks – from the lack of charging points to electric powertrain innovation and the need for increased connectivity and driver assistance – but the requirements will be different and additional investment will be necessary.

In the short-run, there is likely to be some first-mover advantage for premium truck brands like Scania to provide zero-emissions trucks at premium prices, but costs will need to fall for widespread adoption and – as with passenger cars – the differentiators for brands will shift towards driving technology.

Connectivity & Autonomous Vehicles

One thing to bear in mind when considering the growth of EVs is their performance relative to ICE vehicles. Although EVs are currently do not currently have a significant advantage, many believe that in the future EVs will have higher lifetime mileage, last longer and better retain their value.

This is likely to mean higher financing revenue as more customers choose to pay off their cars over a longer period and, more importantly, it might mean a lower overall volume of purchases, and a higher dependence on services to fill the revenue gap.

Similar to other tech-based industries, add-ons and software subscriptions are likely to become a significantly more important part of business models. Tesla, for example, charges US$10,000 for its “full self-driving” add-on, which its CEO, Elon Musk, has said could ultimately reach a value of US$100,000 – more than the value of the original car – and be spread across the life of the car in a subscription model. The value potential of this type of innovation is clear, but the investment and innovation requirements will be significant.

The obvious extension to this is autonomous driving. Increasingly it is becoming clear that the road to autonomous driving will involve small increments rather than moonshot investments like those of Uber, Google and Apple - which are still a long way from having a solid business case.

This gives an opportunity to existing OEMs to slowly increase from driver assistance and partial automation to high automation, and ultimately full automation, as issues with risk-sharing and liability are resolved.

The level of connectivity may also be one reason to question the rise of Chinese brands outside of China. Given the level of data collection required and the importance of trust in the software, some consumers outside of China may be reluctant to purchase Chinese brands given the state of relations between China and the West.

Focus of Investment Changing (R&D versus Marketing)

Judging by recent announcements, CAPEX and R&D investment is set for a boom. Recently, however, CAPEX has been stable as a proportion of revenue. R&D investment increased modestly with relatively high growth in the last year and is now equivalent to 4.6% of revenue for listed automobile brands. This is equivalent to an absolute increase of US$700 million between 2019 and 2020 (0.6% growth compared to 2019). These increases are positive signs, but more will be needed to take advantage of the opportunities the industry is facing.

(% of Revenue)

R&D investment changes dependent on the OEM – in general, German brands have been investing robustly in preparation for the new changes; beyond even what fast-growing Tesla spends. Audi, BMW and Volkswagen all increased R&D spending as a proportion of revenue last year, and have an average investment rate of 6.6% - higher than the average for the industry.

No entanto, esse investimento parece estar custando. O investimento em marketing está caindo rapidamente, e este ano diminuiu como uma proporção de receita (6,5%, em média, em 2020, em comparação com 8% em 2016) para pelo menos os 5 th Consecutivo e que se rebimizamos, mas é o que se rebimiza, mas é o que se rebimiza, mas é o que se rebimiza, mas é o que se rebimiza, mas é o que se rebimiza e, em parcialmente, é que há muito tempo, e é considerado um pouco, e que se rebimizamos, que é considerado um pouco, e que se rebimizamos. Os consumidores precisarão ser guiados através da transição de EV e-apesar da estratégia fóbica de publicidade da Tesla-aquelas marcas que têm alto reconhecimento da marca e, portanto, alta disponibilidade mental, serão as que tomarão participação de mercado. Construir relacionamentos com futuros clientes será tão importante quanto a própria tecnologia. (por valor) Em 2019 a 11% em 2030, de acordo com o McKinsey Mobility Center. Valor. O valor total das 20 principais marcas de componentes de automóveis mais valiosos aumentou 32,5%, em comparação com um aumento de 4,4% para as 100 marcas de automóveis mais valiosas. A China, com seu mercado de EV em expansão, é novamente o artista mais forte, com o valor das marcas de componentes de automóveis chineses com base em 269%, para US $ 2,5 bilhões. Esses chips viram uma escassez enorme que ainda está afetando o mercado. Os carros têm mais de 1.000 peças diferentes que dependem de semicondutores e das marcas capazes de manter seu suprimento de maneira eficaz (como a Toyota - um aumento de 8,1% em valor da marca) provaram ser mais bem -sucedidos do que aqueles que não são (não é de um MODEMENT MODEMENTO, MOLEMENTO RETEMING RETERNATEMENTO, MOLEMENTO RETEMENTO, MOLEMENTO RETEMENTO, MOLEMENTO RETEMENTO, MOLEMENTO RETEMENTO A REVISTA REMOTEMENTO, RETEMENTO A REVISTA REVERTION | Um serviço (MAAs) fica generalizado. O loop de Las Vegas da Tesla, que estreou na CES no início deste ano, mostra como isso pode ser no futuro, mas já existem muitas marcas estabelecidas nas cidades em todo o mundo. Diferentemente das marcas tradicionais de serviços de aluguel de carros, há pouca ou nenhuma escolha sobre o tipo de modelo, e os carros são usados por períodos muito mais curtos de tempo. Sob algumas estimativas, 1 em cada 10 carros novos poderiam ser de propriedade de empresas compartilhadas até 2030. A influência na preferência do modelo pode, portanto, ser significativa e, dada a natureza de compartilhamento do produto, também pode deprimir as vendas gerais de volume.

This is partly an outcome of the pandemic, and we expect there to be some rebound, but there is a long-term trend, and in many ways seems short-sighted. Consumers will need to be guided through the EV transition and – despite the advertising-phobic strategy of Tesla – those brands that have high brand awareness, and therefore high mental availability, will be the ones that take market share. Building relationships with future customers will be just as important as the technology itself.

Focus Change for Auto Components Brands

The technology and parts required for EVs will be significantly different to those for traditional ICE vehicles and will create a huge change of focus for auto components brands.

ICE components such as engines, transmissions and fuel injection systems will all fall in importance, from 26% of the market size (by value) in 2019 to 11% in 2030, according to Mckinsey Mobility Centre.

The value of emerging components such as hybrid transmissions, batteries, head-up displays, and interiors are expected to increase from 26% to 52% - pushing “stable” components down from 48% to 37% of the total, as the value of emerging components becomes a higher part of overall value.

The prospect of this growing value share for components has been pushing up brand values among auto components brands. The total value of the Top 20 most valuable auto components brands is up 32.5%, compared to a 4.4% increase for the Top 100 most valuable automobile brands.

Although volumes and revenues in the last two years have been depressed, auto components brands are taking big bets on EV, and they are forecast to remain resilient. China, with its booming EV market, is again the strongest performer, with the value of Chinese based auto components brands soaring 269% to US$2.5 billion.

Unfortunately for automobile brands, however, the new advancements in EVs and connectivity require not only on traditional parts suppliers but rely on semiconductors. These chips have seen huge shortages that are still affecting the market. Cars have over 1,000 different parts that rely on semiconductors, and those brands that are able to maintain their supply effectively (like Toyota – up 8.1% in brand value) have proven to be more successful than those that do not (Volkswagen – down 12.7%).

Mobility as a Service & Car Rental Services Comeback

Technology is not only taking over model design but also business models, as Mobility as a Service (MaaS) become widespread. Tesla’s Las Vegas Loop, which premiered in CES earlier this year, shows what this could look like in the future, but there are already many established brands in cities worldwide.

Zity, ShareNow, GoTo, ZipCar and many other similar apps have bought large fleets of cars, particularly EVs, to match demand. Unlike traditional car rental services brands, there is little to no choice over model type, and the cars are used for much shorter periods of time.

These brands are likely to become large customers of the traditional OEMs – influencing model development since these applications tend to favour small three and five-door electric vehicles for city use. Under some estimates, 1 in 10 new cars could be owned by sharing companies by 2030. The influence on model preference could therefore be significant and, given the sharing nature of the product, could also depress overall volume sales.

Isso traz desafios e oportunidades aos serviços tradicionais de aluguel de carros. Mais investimentos precisarão ser feitos em frotas eletrizantes - como a Hertz está tentando fazer com sua ordem de 100.000 Teslas no final de 2021.

2021 foi um bom ano para a marca de aluguel de carros e as marcas e previsões para o setor. Para sustentar o crescimento do valor da marca, investir em tecnologia para competir com novas marcas de maas e uma atualização do que muitos percebem como identidades tradicionais de marca serão necessárias.

Car Dealerships, Online Sales & New Used Car Brands

Embora não seja um ranking nos relatórios da indústria automotiva financeira da marca este ano, as concessionárias não foram poupadas de interrupções em seu setor. Os VEs, sendo uma proposta mais cara, criarão pressão descendente sobre as margens, pois as concessionárias tentam vendê-las a preços competitivos. Os requisitos de manutenção serão, portanto, mudam de foco, com o suporte ao software em particular devido a se tornar cada vez mais importante. No entanto, muito disso será feito de "ao ar" diretamente por OEMs-reduzindo o potencial de valor para concessionárias. Crie potencialmente oportunidades para novas marcas assumirem o controle. A dependência de vendedores individuais com metas de vendas reduz a confiança e aumenta o aborrecimento, assim como os atrasos que são inevitáveis ao assinar contratos. Da mesma forma, para os OEMs, a cadeia de vendas os coloca longe do consumidor e reduz o controle sobre a experiência da marca. No início de 2021, a Volvo anunciou que todos os veículos elétricos puros estariam disponíveis apenas para compra on -line. Existem benefícios significativos não apenas no crescimento da margem, mas também no gerenciamento de marcas, pois as vendas on -line fornecem um controle mais detalhado sobre os relacionamentos com os clientes sem a necessidade de investir pesadamente em infraestrutura física. Apesar disso, a maioria dos OEMs está adotando uma abordagem híbrida com questões regulatórias para a transição completa para o on-line ser um bloqueador-pois as vendas diretas dos OEMs para o consumidor são restritas em algumas jurisdições. Carvana, Vroom, Carvago, Cinch, Auto1, Cazoo, Kavak, Carnext, Carro e Amaris estão todos na longa lista de start-ups que recebem grandes quantidades de financiamento e fazendo um grande número de aquisições. Os consumidores confiam cada vez mais plataformas on -line durante todo o processo de compra e venda para vendas de carros novas e usadas, e a indústria está crescendo em um ritmo forte.

After-market parts and servicing are likely to reduce in importance as the number of parts necessary for EVs decrease and their reliability increases. The requirements on servicing will therefore change in focus, with software support in particular due to become increasingly important. However, much of this will be done “Over-The-Air” directly by OEMs – reducing the value potential for dealerships.

These changes will create pressures for training, with dealers’ existing knowledge being much more focused on ICE vehicles, however, there is a clear role for OEM brands in this transition.

In addition to these trends, the rise of online sales will increase the strain on traditional dealerships, and potentially create opportunities for new brands to take over.

Purchasing cars in traditional dealerships is generally a high-anxiety, low-trust and low-enjoyment experience. The reliance on individual salespeople with sales targets reduces trust and increases annoyance, as can the delays that are inevitable when signing contracts. Similarly, for OEMs the sales chain puts them far from the consumer and reduces control over brand experience.

The chain is ripe for disruption, and it is being disrupted. In early 2021, Volvo announced that all pure electric vehicles would only be available for purchase online. There are significant benefits not only in margin growth but also in brand management as online sales provide closer control over relationships with customers without the need to invest heavily in physical infrastructure. Despite this, most OEMs are adopting a hybrid approach with regulatory issues for the full transition to online being a blocker – as direct sales by OEMs to the consumer is restricted in some jurisdictions.

However, non-OEM online retailers are booming. Carvana, Vroom, Carvago, Cinch, Auto1, Cazoo, Kavak, CarNext, Carro, and Amaris are all on the very long list of start-ups receiving large amounts of funding and making a large number of acquisitions. Consumers are increasingly trusting online platforms through the whole purchase and sale process for new and used car sales, and the industry is growing at a strong pace.

Então, o que isso significa para as marcas? A produção se tornará a próxima fonte-chave de diferenciação nessa base. por moradores da cidade que valorizam carros menores e estão interessados em um posicionamento mais focado no verde. À medida que os VEs se tornam mais mainstream, essas não serão as principais características que os consumidores procuram em todos os mercados, e as mensagens da marca e os processos de produção devem tomar nota disso. Os requisitos desses novos tipos de clientes (ou seja, estritamente B2B) precisarão ser investigados adequadamente. A capacidade de trocar desses avanços será limitada se todas as outras marcas estiverem fazendo a mesma coisa. Portanto, deve -se ter uma consideração cuidadosa para garantir que a promessa da marca seja crível, sustentável e diferenciadora. As plataformas para a maioria dos OEMs precisarão ser aprimoradas, e a confiança entre os clientes precisará ser recebida por meio de departamentos de atendimento ao cliente bem resumidos e responsivos e políticas adequadas para queixas e retornos.

Prepare for the next "Green" Challenge - Car production rather than drivetrain type

As EVs become more mainstream, green credentials based solely on the powertrain will become less convincing. Production will become the next key source of differentiation on this basis.

Brands that are able to convincingly explain the sustainability of their production process – from the restriction on the use of rare minerals to the incorporation of recycled material – will be the most successful, particularly in the premium segment.

Avoid over-focus on "first-mover" Urban consumers

The current EV market is being driven by city-dwellers who value smaller cars and are interested in a more green-focused positioning. As EVs become more mainstream these will not be the primary characteristics that consumers look for in all markets, and brand messaging as well as production processes should take note of that.

Car sharing will also grow in importance and be a key driver of demand for some models. The requirements of these new customer types (i.e. strictly B2B) will need to be adequately investigated.

Avoid copy-cat brand positioning

The growth of EV has led to the proliferation of sub-brands with futuristic tech-influenced names and advertising strategies emphasising technological advances. The ability to trade off of these advances will be limited if all other brands are doing the same thing. Careful consideration should therefore be made to make sure the brand promise is believable, maintainable and differentiating.

Continue to prepare for online sales

Online sales will continue to grow. Platforms for most OEMs will need to be improved, and trust among customers will need to be garnered through well-resourced and responsive customer service departments and adequate policies for complaints and returns.

Summary brand metrics needed more than ever

Finalmente, à medida que os requisitos da indústria mudam rapidamente as marcas precisam controlar o que estão investindo, o que as pessoas pensam delas e se essas percepções estão sendo transferidas para o desempenho financeiro. Um scorecard equilibrado dos benchmarks de força da marca é a maneira mais apropriada de fazer isso e deve ser adotada o mais amplamente possível. HAIGH